Mohammed Omran, Ph.D.

“History repeats itself, first as tragedy, second as farce,” wrote Karl Marx in “The Eighteenth Brumaire of Louis Bonaparte”. While he was dissecting a specific political moment in the 19th century, his observation carries a striking relevance for contemporary economic policymaking. When the deep-seated structural weaknesses of an economy are left to simmer unresolved, financial pressures have a way of returning, often wearing a new mask but following a painfully familiar pattern. The escalation of war in the Gulf between the U.S., Israel, and Iran is not merely a regional security concern. It also constitutes an economic shock with direct implications for Egypt. Energy markets, investor sentiment, remittance flows, and trade routes are all transmission channels through which regional instability affects the Egyptian economy.

Recent developments in Egypt’s foreign exchange market have therefore revived an important question: does the latest movement in the Egyptian pound signal the beginning of another cycle of devaluation? While some are tempted to view it as such, doing so would be a misreading, as this current volatility likely represents a temporary overshooting driven by regional uncertainty rather than a shift in economic fundamentals. The central point is not whether Egypt is facing an imminent crisis, but whether it risks re-entering a familiar cycle if current events impede reform momentum. In other words, it is a reminder that if structural adjustment is not completed, we risk the tragedy of history repeating itself yet again.

Egypt’s macroeconomic position is significantly firmer than it was a few years ago. Foreign exchange reserves are higher, external liquidity has improved, and investor interest has returned. Yet, even with these gains, this current episode should be seen as a clear warning signal. It suggests that while Egypt has made real progress in stabilizing its macroeconomic environment, the economy has not yet built the “structural immunity” needed to handle external shocks without slipping back into familiar financial pressures. This is not just about policy effort. It reflects a deeper, unfinished transformation.

Too often, early signs of stability are treated as an endpoint rather than what they really are: a temporary pause in a much longer journey. Policymakers ease off too soon, celebrate too early, and end up confronting the same vulnerabilities all over again. In today’s increasingly unforgiving global environment, resilience does not come from short-term stability—it must be built to last.

- Regional Conflict and Transmission Channels to Egypt

The ongoing tensions in the Gulf introduce a multi-dimensional external shock with several transmission channels affecting the Egyptian economy.

First, despite recent gas discoveries, Egypt remains a net importer of petroleum products. A sustained increase in global oil prices would widen the trade deficit and place additional pressure on the fiscal balance, particularly through higher energy subsidy costs.

Second, disruptions to maritime routes—especially around the Strait of Hormuz and the Red Sea—could indirectly affect Suez Canal revenues. Given that the Canal represents a critical source of foreign currency, any sustained decline in traffic or rerouting of global shipping would have immediate balance-of-payments implications.

Third, heightened geopolitical risk typically leads to a deterioration in global risk appetite. Emerging markets, including Egypt, often experience capital outflows under such conditions, particularly in the form of short-term portfolio investments. This can exert pressure on the exchange rate and domestic liquidity conditions.

Fourth, and perhaps most critically, a prolonged regional crisis could disrupt the single most important lifeline of the Egyptian economy: remittances. With record inflows exceeding $41.5 billion in 2025, largely from Egyptian workers in the Gulf, any regional economic slowdown could turn a manageable “warning signal” into a much harsher fiscal reality. Remittances are not just a line item in the balance of payments; they are the private safety net for millions of Egyptian households, and their volatility directly impacts domestic consumption, social stability, and foreign currency availability. Taken together, these factors illustrate that exchange rate pressures are not merely numerical adjustments but are deeply embedded in the interaction between external geopolitical shocks and domestic structural fragility.

- Exchange Rate Adjustments, Structural Pressures, and the Currency as a Warning Signal (2016–2026)

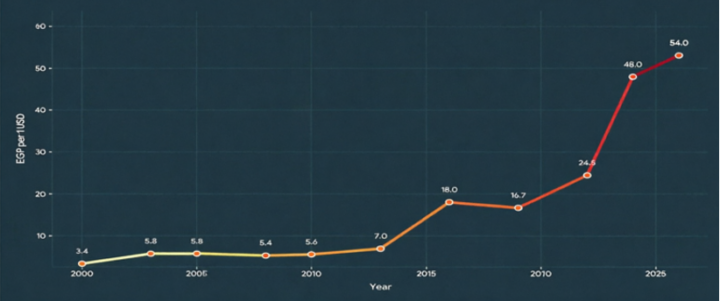

To understand current exchange rate dynamics in Egypt, it is essential to revisit the adjustment cycle that began in 2016. The decision to liberalize the exchange rate—moving the pound from approximately EGP 8.8 to nearly EGP 18 per US dollar—marked a decisive shift in economic policy. Supported by an IMF-backed reform program, the move helped restore investor confidence, rebuild foreign exchange reserves, and re-establish Egypt’s access to international capital markets.

Figure 1 - Historical Evolution of the EGP/USD Official Exchange Rate (2000–2026), highlighting major devaluation episodes and recent overshooting.

Source: Central Bank of Egypt (CBE) Historical Data and International Financial Statistics database, International Monetary Fund (IMF).

In the years that followed, macroeconomic indicators improved: growth recovered, reserves increased, and Egypt became a key destination for high-yield-seeking portfolio inflows. However, this apparent stability masked a growing structural vulnerability. The economy became increasingly reliant on short-term capital flows, commonly referred to as “hot money,” which are highly sensitive to global financial conditions. As global interest rates rose and investor sentiment toward emerging markets weakened, these flows reversed, exposing the fragility of the financing model and placing renewed pressure on the exchange rate.

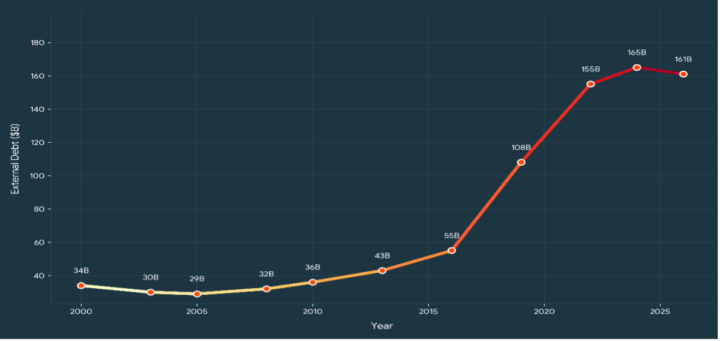

At the same time, external sovereign debt increased to approximately $160–165 billion. More critically, a significant portion of this debt is concentrated in short- and medium-term maturities, creating persistent roll-over risks and sustained demand for foreign currency. This dynamic has effectively tied exchange rate stability to the continuous availability of external financing, rather than to underlying productivity or export competitiveness.

Figure 2: Trajectory of Egypt’s Total External Debt (2000–2026), showing the accelerated accumulation in the post-2016 period.

Source: Central Bank of Egypt External Position Reports and International Monetary Fund (IMF), International Financial Statistics (IFS).

These accumulated pressures became more visible between 2022 and 2024, when the exchange rate underwent a series of sharp adjustments. After prolonged attempts to manage the currency within a relatively narrow range, the Egyptian pound depreciated significantly in early 2024, eventually reaching levels in the mid-to-high forties against the US dollar. This adjustment reflected not only the delayed correction of imbalances but also the interaction between domestic vulnerabilities and tightening global liquidity conditions.

The period from mid-2024 to early 2026 saw some relative stabilization. This was not solely the result of structural improvement, but rather the outcome of a combination of exceptional and policy-driven factors. The “Ras El Hekma” investment deal, which concluded in early 2024, provided a substantial, one-off injection of foreign currency, easing immediate pressures on the balance of payments. At the same time, the alignment of the official and parallel exchange rates encouraged a significant return of remittance flows through formal channels, strengthening foreign currency inflows.

However, this recent stabilization of the Egyptian pound should not be interpreted as a definitive resolution of underlying challenges. Rather, it represented a temporary equilibrium that remained contingent on continued inflows and relatively stable external conditions. This moment of equilibrium has now faded as the region faces major geopolitical uncertainty. Specifically, the exchange rate has begun to climb once again, with the pound recently overshooting its fundamental value to reach the low fifties against the dollar. This shift is already affecting investor sentiment, energy prices, and potentially remittance flows, serving as a reminder that the economy remains highly sensitive to external shocks. The policy challenge, therefore, is not merely to defend the current level of the exchange rate, but to address the structural factors that make such pressures recurrent.

It is important to clarify that the distinction between a warning signal and a crisis lies in the current macroeconomic buffers. With foreign exchange reserves exceeding $52 billion, Egypt possesses the “firepower” to navigate this temporary overshooting without slipping into a disorderly collapse. However, this strength should be viewed as a defensive shield, not a permanent cure. If the geopolitical situation remains tense and policymakers fail to use this “breathing room” to implement structural reforms, specifically increasing domestic savings and reimagining debt, we risk seeing the current volatility transition from a manageable shock into a potential systemic crisis.

- Persistent Structural Vulnerabilities

Despite recent stabilization efforts, several structural weaknesses continue to constrain Egypt’s economic resilience.

Inflation remains closely tied to exchange rate movements. Because Egypt depends heavily on imported essential commodities, even minor currency fluctuations are immediately transmitted into domestic prices, making the stability of the pound a matter of social security as much as economic policy. While it is still too early to measure the full extent of the current inflationary wave, the government's immediate increase in fuel prices is expected to exert significant upward pressure on transportation costs and the distribution of all goods. This surge in logistical expenses will likely impact the entire supply chain, further straining the purchasing power of those most dependent on price-sensitive essential commodities.

External financing dependence is another critical issue. Short-term investments are great when the world is calm, but they are the first to run during a global tightening cycle or a geopolitical storm, forcing policymakers back into defensive maneuvers. This “hot money” creates a false sense of security during the good times, but its sudden exit creates a liquidity vacuum that can paralyze the foreign exchange market. We are learning that you cannot build a stable house on a foundation of capital that can be withdrawn with a single click in a London or New York trading office. True stability must come from “sticky” capital in the form of foreign direct investment that builds factories, employs people, and stays in the country for decades.

Moreover, the structure of external debt amplifies these risks. High debt levels combined with relatively short maturities generate constant refinancing needs, placing pressure on reserves and limiting policy flexibility.

These vulnerabilities imply that external shocks—such as war in the Gulf—can have disproportionately large domestic effects, even in the absence of fundamental macroeconomic deterioration. For Egypt, this is a double whammy. On one hand, it makes essential imports like petroleum products and wheat more expensive, widening the trade deficit. On the other hand, it scares off global investors who see the entire region as a “danger zone,” leading to a retrenchment of capital back to safe-haven assets. This dual pressure explains why exchange rate volatility has intensified in recent weeks, even when the immediate trigger lies outside Egypt.

In such a context, it is important to look at what Egypt can do to ensure that its exposure to external shocks does not translate into a further currency devaluation and a consequent impact on its society. The risk here is that a prolonged conflict may turn these manageable vulnerabilities into a self-reinforcing crisis. As long as the regional “danger zone” persists, the persistent drain on reserves and the upward pressure on inflation will test the limits of social stability. This suggests that the window of opportunity provided by recent stabilization is narrowing; the longer the external shock lasts, the more urgent the need becomes to transition from a strategy of survival to a strategy of structural immunity.

- The Defensive Shield: Buffering Near-Term Shocks

Before turning to long-term immunity, it is important to recognize the defensive walls currently protecting the Egyptian economy. Chief among them is the recovery in the foreign exchange reserves, which have climbed back to a robust position, holding steady above the $52 billion mark. This is not just a psychological comfort; it is a massive operational tool. It gives the Central Bank a greater capacity to smooth temporary volatility, meet demand for foreign currency, and avoid the acute shortages that previously disrupted production and trade.

Alongside reserve accumulation, the recent moderation in inflation has provided some policy space. Inflation was in the 12–13% range by early 2026, down from around 24% a year earlier. Lower inflation eases immediate pressure on households and gives the Central Bank more room to calibrate its response to external shocks. However, recent domestic policy adjustments add further complexity to the near-term outlook. The decision to increase fuel prices effected on 10 March—while fiscally necessary—comes at a particularly delicate moment, coinciding with renewed exchange rate pressures and elevated regional uncertainty. This combination is likely to reintroduce inflationary pressures through cost-push channels, particularly affecting transportation, production, and food prices. Early indicators already suggest a tightening in the agricultural sector, where the increased cost of energy is being reflected in fertilizer prices and irrigation costs. While the exact magnitude of this impact will only become clear as the “roll-over” effect permeates the supply chain, the immediate hike in logistics and input costs is expected to place renewed upward pressure on basic food commodities, further straining the purchasing power of the most vulnerable.

In this environment, expectations of a continued monetary easing cycle may need to be reassessed. While recent trends before the current regional war had pointed toward gradual disinflation and potential rate cuts, emerging inflation risks and external volatility may require a more cautious stance.

These buffers are important, but they also have limits. While $52 billion is an important sum, it is not infinite. In a global economy defined by sudden shifts and “Black Swan” events, a reserve can be depleted faster than it was built if the underlying demand for dollars remains structurally high. We have seen in the past how quickly billions can vanish when trying to defend a currency against a global tide. Following the outbreak of the Russia-Ukraine war in 2022, Egypt witnessed an aggressive “bleeding” of liquidity, where billions in portfolio investments exited the country in a matter of weeks, significantly exhausting a reserve that stood at roughly $41 billion at the time. While the current reserve of $52 billion provides a much larger “defensive shield”, this shield is not endless. Recent data indicate that these reserves cover roughly 6 to 6.5 months of imports, underscoring that in a high-stress scenario—where regional conflict persists and import costs spike—the “survival horizon” of these reserves could narrow from years to mere months. This historical parallel reinforces the argument that the current stability is a temporary window that must be used to build structural immunity before the next inevitable tide.

Similarly, the cooling of inflation is a delicate victory. Because Egypt remains so heavily dependent on imported food, fuel, and raw materials, its domestic price stability is essentially “on a leash” held by the exchange rate. As long as it is an import-heavy nation, the country is essentially importing the world’s inflation.

In the current environment, policymakers face the challenge of managing external shocks while preserving macroeconomic stability. Several short-term priorities emerge. Maintaining exchange rate flexibility is essential to avoid the build-up of imbalances as attempts to artificially stabilize the currency can deplete reserves and delay necessary adjustments. At the same time, preserving foreign exchange reserves remains critical, requiring a careful prioritization of foreign currency toward essential imports and strategic sectors.

Inflation management, meanwhile, should focus on targeted interventions rather than broad-based controls. Protecting vulnerable households from price shocks, especially in food and energy, can help maintain social stability.

Finally, the necessity of safeguarding remittance flows, which reached a record $41.5 billion in 2025, becomes even more critical if the Gulf region enters a period of economic softening. To protect this vital source of foreign currency, Egypt must ensure that official banking channels remain the most attractive and competitive option through high-yield financial products and low-cost transfer mechanisms. By proactively maintaining the incentive for formal transfers, the government can prevent a return to informal markets and ensure that this social and economic lifeline remains secure even during a prolonged regional downturn.

- The Strategy of Immunity: Long-Term Structural Reform

Short-term stabilization is necessary, but it is not enough. If reserves are the economy’s short-term shield, then structural reform is what builds its long-term immunity.

Such reform spans multiple dimensions: creating a more attractive investment climate, diversifying exports, reducing bureaucratic obstacles, strengthening human capital, and improving health and education systems. These are all critical to building a resilient economy. However, here we focus on two fundamental enabling factors that have an outsized impact on Egypt’s vulnerability to external shocks: domestic savings and the management of external debt.

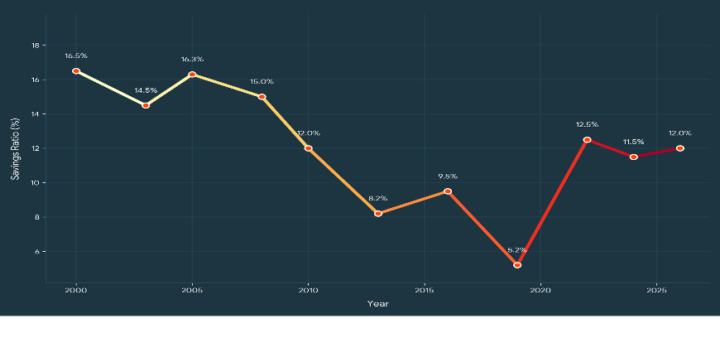

First, Egypt must raise its national savings rate, as mobilizing domestic resources is essential for sustainable growth. Historically, Egypt’s domestic savings have been modest, standing at around 11-12% of GDP as an average since 2000, significantly lower compared to peer nations in emerging markets, particularly those in East Asia, such as Vietnam or Thailand, where savings rates often exceed 30%, providing a stable, internal engine for industrial growth. Even in Latin America, economies like Chile have managed to mobilize higher levels of domestic capital to reduce their reliance on external financing. This creates a chronic “financing gap”: the difference between what the country needs to invest to grow and what it saves. Filling this gap through foreign borrowing makes the economy highly vulnerable: insufficient domestic savings effectively outsource economic stability to foreign creditors. To reduce this vulnerability, Egypt should aim to raise its national savings rate to 20–25% of GDP, or even 30% as achieved historically in high-growth Asian economies.

Figure 3: Trends in Egypt’s Gross Domestic Savings as a Percentage of GDP (2000–2026).

Source: World Development Indicators (WDI), World Bank, and Ministry of Planning and Economic Development (Egypt).

Achieving this in the current high-inflation environment requires a fundamental transition from a model of consumption-led growth to one driven by domestic capital formation through a series of integrated structural shifts. This requires the state to prioritize deepening financial inclusion by leveraging digital banking and mobile wallets to capture vast pools of informal savings. By integrating these resources into the formal financial system, the banking sector can secure the more stable, long-term liquidity necessary for investment. Furthermore, the introduction of inflation-indexed savings products is essential to protect the purchasing power of Egyptian households, providing a meaningful incentive for long-term deposits over immediate consumption or “hedging” through unproductive assets like gold or foreign currency. Finally, these efforts must be supported by robust capital market reforms that provide diverse investment vehicles beyond traditional real estate. Strengthening these markets allows for a more efficient mobilization of domestic resources into productive sectors of the economy, effectively reducing the “crowding out” effect often caused by government debt and ensuring that domestic capital remains a primary driver of national economic security.

Second, Egypt must improve the structure, not just the size, of its external debt. As noted earlier, the real danger lies not only in the total amount of external debt (which stands at $163 billion) but in its structure. Much of this debt is short- and medium-term, creating a “roll-over risk”: a constant scramble for liquidity just to pay interest and principal. This pressure is the primary drain on reserves and a key reason the exchange rate remains so sensitive.

Addressing this requires a strategic pivot in debt management that goes beyond simply paying the bills. Egypt must seriously negotiate to extend maturities, aligning repayment obligations with the long-term nature of its development projects. A credible path forward requires Egypt to move beyond passive debt servicing toward a strategic restructuring framework—leveraging growing international concern over developing-country debt vulnerabilities to negotiate maturity extensions, debt reprofiling, and debt-for-climate swaps aligned with SDGs commitments, thereby easing near-term pressures while anchoring long-term sustainability. These mechanisms allow the country to reduce debt burdens by committing to spend the same funds on domestic development priorities—renewable energy, education, or healthcare—in local currency, effectively recycling debt into the economy rather than sending hard currency abroad. When paired with structural reforms such as export diversification, improving the investment climate to attract long-term foreign direct investment, and removing bureaucratic barriers for small and medium enterprises, the debt becomes far more manageable, and the economy gains resilience.

- Conclusion: Moving Beyond Reactivity Toward Economic Immunity

The recent pressure on the Egyptian pound should not be misinterpreted as evidence of an imminent crisis. It is better understood as an important warning signal: a reminder that Egypt’s stabilization gains, while substantive in recent years, remain incomplete. The current war in the Gulf demonstrates how rapidly regional shocks translate into domestic economic pressure, proving that resilience cannot be built solely through short-term stabilization.

Egypt has made important progress in recent years. However, sustaining this progress requires a shift toward deeper structural reform: strengthening domestic savings, improving debt management, reducing reliance on volatile external flows, and supporting more productive, durable sources of growth.

Ultimately, whether the pound remains at these levels or relaxes as regional pressures ease, the core lesson remains unchanged. An exchange rate that overshoots due to external shocks is a symptom of an economy that has not yet completed its structural transformation. We must not let a potential “relaxation” of prices lead to policy complacency; instead, we must use this warning to accelerate the shift toward deeper structural reform—one that strengthens domestic savings, improves debt management, and reduces reliance on volatile external flows.

However, to prevent the economy from repeating the familiar cycle of external shocks and emergency interventions, we must transition from a “strategy of survival” to a “strategy of immunity.” The challenge is not simply to avoid the next crisis, but to build an economic model robust enough to withstand it—whenever it comes.

The views expressed in this article are solely those of the author and do not necessarily reflect the positions, policies, or views of any affiliated institution or its leadership, including its president and executive board.

The views represented in this paper are those of the author(s) and do not necessarily reflect the views of the Arab Reform Initiative, its staff, or its board.