Introduction

From 2022 to 2024, Egypt suffered from a deep sovereign debt crisis that had various effects extended to all sectors of the Egyptian economy. The crisis, and the subsequently high debt payments over the past two years, led to dollar scarcity, successive currency devaluations, and a severe import crisis; these effects further resulted in inflation rising to record levels of over 40% year-on-year in June 2023. The debt crisis is a direct product of the heavy borrowing policies that began in Egypt after 2016 and took root after the devaluation of the Egyptian pound in November 2016. The devaluation made Egyptian bonds and treasury bills more attractive to international capital, especially to portfolio investors or hot money, which in addition to global variables has continuously exposed Egypt to outflows. Egypt has suffered three crises driving out hot money investors: in 2018 with the Fed raising interest rates; in 2020 with the first wave of the COVID-19 pandemic and the global economic uncertainty of that time; and in 2022, after the Russia-Ukraine war, which was the final nail in the coffin for Egypt’s reliance on hot money to keep the exchange rate and inflation at acceptable levels.

The scope of the crisis began to widen at the end of 2021 due to Egypt’s debt payments, as debt installments without interest jumped from approximately $10 billion in 2019 to about $21.7 billion in 2022, according to the Central Bank of Egypt (CBE) data. During the three years, from the beginning of 2021 to the end of 2023, Egypt was in dire need of the Gulf region support, long-delayed partly for political reasons. The relative independence with which Egypt tried to formulate its foreign policy toward Libya, for example, led to it being on the opposite side of the issue from the UAE, the largest investor in Egypt. Saudi Arabia was preoccupied with the aftermath of the murder of journalist Jamal Khashoggi and its relationship with the US, and Egypt had taken a largely neutral stance on the war in Yemen by not getting directly involved.

But by 2022, Egypt was in dire need of financial rescue to control the consequences of its economic crisis. At the end of 2021, it began negotiations with the International Monetary Fund (IMF) and other regional partners on a major financial bailout. However, the IMF only approved a $3 billion loan beginning in 2023. The loan agreement obligated the government to raise another $14 billion through a number of other financings, sell several state-owned assets, and secure Gulf support. The process of securing Gulf support has not been easy, and many supposed Gulf acquisitions of various Egyptian companies have stalled.

The Gulf support, slightly delayed in 2023 during which the economic crisis intensified, came in February 2023 with the Ras al-Hikma deal, which guaranteed new dollar inflows to the Egyptian government estimated at $24 billion, in addition to the UAE’s waiver of $11 billion of its deposits in the CBE.

In this paper, which begins by emphasizing the dual nature (political and economic) of Gulf support, especially after 2013, we examine the Gulf itself and its premises for this support, both economic and political. The paper will attempt to draw a broader picture of Gulf investments in Egypt and their role in the Egyptian economy, especially in relation to the Egyptian private sector in the Gulf, as well as how the nature of capital accumulation in Saudi Arabia and the UAE – the two major Gulf countries – affects the structure of the Egyptian economy in general.

In the first section, we will review recent acquisitions and examine why Saudi Arabia and the UAE are interested in acquiring these types of assets and the reasons behind the major financial support – namely the Ras Al-Hikma deal – was delayed, and how it finally materialized.

In the second section, we explore the complex relationship between capitalism in Egypt and capitalism in the Gulf. The organic link between the two has deepened over the past decade through a regional structure of economic accumulation, in which the Gulf has played an important role through its oil surpluses. The third section looks at what Saudi Arabia and the UAE aim to gain from these acquisitions.

Gulf Acquisitions from April 2022-April 2024

The wave of acquisitions of Egyptian companies by Gulf sovereign funds began in April 2022 with the Abu Dhabi Developmental Holding Company (ADQ), a subsidiary of the Abu Dhabi Sovereign Fund, buying stakes in five Egyptian companies listed on the Egyptian Exchange in a one-day transaction. The acquisitions included a 32% stake in Alexandria Container and Cargo Handling Company, valued at $186 million, and the government’s 12% stake in Fawry Digital Payments, valued at $68.6 million. ADQ also acquired 18.5% of Commercial International Bank Egypt (CIB) in a $911 million transaction; the stake was previously held by Al Ahly and Banque Misr, Egypt’s largest state-owned banks. The ADQ also bought part of the Ministry of Finance’s 20% stake in Misr Fertilizers Production Company, worth $266.6 million, and the National Investment Bank’s 21.52% stake in Abu Qir Fertilizers, worth $391.9 million.

The first wave of acquisitions drew much criticism from financial experts due to the low value of the shares, as they were significantly undervalued on the stock exchange. These were the prices at which the majority of the acquisitions were carried out and were explained due to the urgent need for dollars to face the severe currency shortage.

In August 2022, another wave of Saudi acquisitions began, during which the Saudi Egyptian Investment Company, a subsidiary of the Saudi Public Investment Fund, acquired a number of Egyptian companies, including 25% of e-Finance for Financial and Digital Investments, 19.82% of Abu Qir Fertilizers and Chemical Industries, 25% of Misr Fertilizers Production Company, and 20% of Alexandria Container and Cargo Handling Company.

In June 2023, the ADQ announced its acquisition of stakes in three other Egyptian companies: the National Drilling Company, of which it acquired 25% for $330 million; about 30% of Ethydco; and 35% of the Egyptian Linear Alkyl Benzene Company (ELAB). The three companies were not listed on the stock exchange, but were instead part of the “pre-IPO” fund established by the Egyptian Sovereign Fund that prepares companies before they are listed on the stock exchange; in the current phase of the acquisitions, the Egyptian Sovereign Fund plays the role of an intermediary between Gulf companies and the Egyptian government.

The following table shows the companies acquired by the Saudi and Emirati sovereign funds; it does not include acquisitions made by private sector companies.

Table 1: Recent acquisitions by Saudi and UAE sovereign funds

| Company |

Saudi Arabia |

UAE

Abu Dhabi Sovereign Fund |

Remaining government quota |

Saudi & UAE share (millions) |

| Abu Qir Fertilizers |

19.8% of the company against $ 379 million |

21.5% of the company for $ 393 million |

38.22% |

$771 |

| Misr Fertilizers Production Company |

25% against $370 million |

20% against $ 266 million |

40% |

$636 |

| Fawry |

- |

12.6% of the company’s shares against $ 68.5 million |

22.3% |

$68.5 |

| Commercial International Bank |

- |

18% against $911 million |

- |

$911 |

| Alexandria Container Handling |

20% against $156 million |

32% against $159 million |

42% |

$315 |

| E-Finance |

25% against $391 million |

- |

35% |

$391 |

| Egyptian National Drilling Agency |

-- |

25% against $330 million |

Unknown |

$330 |

| ELAB |

-- |

35% against $170 million |

Unknown |

$170 |

| Ethdeco |

-- |

30% against $280 million |

Unknown |

$380 |

| Total |

$1.3 million |

$2.6 million |

|

$3.9 billion |

Based on the value of recent deals, the UAE through the Abu Dhabi Sovereign Fund and other subsidiaries has been the most active in acquisitions. This could be due to the greater degree of economic diversification that exists in the UAE compared to Saudi Arabia, which has only recently begun to operationalize its economic diversification strategy. But the biggest reason for the UAE’s interest is the nature of the assets that have been put up for sale and the degree of tribal linkage between the Egyptian and UAE private sectors. For example, the CIB deal is an important indicator of that connection. The UAE has five banks operating in Egypt, with more than 418 billion Egyptian pounds (about US$8.5 billion) in assets. Acquiring a large stake of 18% in the largest private sector bank operating in Egypt increases the connection between the banking sectors of the two countries. The UAE is a financial center in the Middle East and the world. Interest in assets in the financial sector, both banking and non-bank financial sectors, is part of the UAE’s financial sector business expansion strategies.

The fertilizer sector is also very important to the UAE, and the Abu Dhabi National Oil Company (a wholly-owned subsidiary of the Abu Dhabi government) has been linking itself to the Egyptian fertilizer sector since the beginning. These ties increased with the gas discoveries in the eastern Mediterranean that ensured the flow of gas to the fertilizer plants in Ain Sokhna that are owned by Orascom. Founded in partnership with the Abu Dhabi National Oil Company in 2018, Orascom has four production facilities across the MENA region, giving it the largest ammonia production capacity in the Middle East. Thus, acquisitions of stakes in state-owned fertilizer companies are strategic to fertilizer production and the petrochemical sector in general, a sector that is highly interconnected in Egypt and the Gulf.

Saudi Arabia’s interests are not much different from those of the UAE. The petrochemical sector in the Gulf has been at the forefront of its industrial sectors, as it is highly correlated with petroleum, so acquiring part of the Egyptian petrochemical sector seems very important to Saudi Arabia.

Among the recently acquired companies are Fawry Digital Payments and e-Finance for Financial and Digital Investments, the two largest e-payments companies in Egypt. Fawry Digital Payments is highly active in consumer finance and microfinance, a sector that is booming in Egypt. Acquiring a company like Fawry Digital Payments makes sense for both the UAE and Saudi Arabia, given their booming digital payments sectors. Expanding into larger markets like Egypt is also highly lucrative for Gulf Cooperation Council (GCC) funds, which in recent years have become more interested in investing in the non-banking financial sector and associated technology solutions.

It was not only state-owned companies that attracted Saudi and Emirati capital in recent acquisitions; the Gulf private sector has been active in acquisitions and mergers since before the crisis in Egypt. For example, Emirati companies have been very active in Egypt’s private health sector by acquiring private hospitals and merging them into two of the largest private sector hospital groups: Cleopatra Hospitals Group and Alameda Healthcare Group, which together account for about 15% of Egypt’s private healthcare market. Since the beginning of 2021, as part of the dissolution and acquisition of The Emirates Towers’ procedures, the Saudi sovereign became a shareholder in the Cleopatra Hospitals Group. Saudi and Emirati companies have also taken a keen interest in the Egyptian real estate sector. For example, an Emirati consortium led by Aldar Properties and the ADQ acquired 85% of the Sixth of October Company for billion Egyptian pounds (about US$122 million); the Sixth of October Company then made an offer to acquire the shares of Madinat Misr for Real Estate Development, one of the largest companies operating in this field. The deal fell through due to disagreements over the valuation of the company’s assets. The Gulf private sector is heavily present in the Egyptian food market through companies such as Saudi Arabia’s Savola, the UAE’s Al Dahra Agricultural Company, Jarir, and others that control the food production process from the farm to the end consumer.

The network of actors in the recent acquisitions in Egypt can be summarized as follows. On the Egyptian side, the Egyptian government is represented by the Egyptian Sovereign Fund, which manages the sale of Egyptian assets. On the other side is the ADSF, which is followed by a number of companies, whether through direct ownership – such as the Abu Dhabi National Oil Company, the ADQ, and Abu Dhabi Ports – or through partnerships with the large private sector companies in the Gulf with close ties to the ruling families – such as Aldar Properties and other Gulf companies that are active in both the Egyptian and Gulf markets. On the other hand, the Saudi Public Investment Fund has been making recent acquisitions in Egypt through the Saudi Egyptian Investment Company, which was established in 2022 to purchase Egyptian assets.

The IMF was present in the 2016 loan, in which the fund’s conditions included a government privatization program that stalled for years before being re-launched in 2022. It is noteworthy that the announcement of the state privatization program in 2018 was aimed at stimulating the capital market and expanding the ownership base of public companies, which differs in philosophy from the current sales of assets to strategic investors, especially from the Gulf. This goal shift could be due to the pressures of the dollar shortage that pushed the government to sell assets to Gulf investors to ensure the dollar inflows needed to finance the deficit, especially given the increase in external debt payments.

The Ras al-Hikma Deal

The Gulf seemed slower to support Egypt during the crisis, specifically from the last quarter of 2022 through the end of 2023. However, rapid geopolitical changes in the region, especially the Israeli war on the Gaza Strip, restored to Egypt a geopolitical importance that was somehow lost during the crisis years. Then came the Ras al-Hikma deal. For the first time during the crisis, Egypt seemed “too big to fail”. This may have been the Egyptian government’s bet from the beginning, and it seems to have paid off in the end.

The ABSF agreed with the Egyptian government to pay $35 billion for the right to develop the Ras al-Hikma area, a 40,600-acre coastal area on the Mediterranean. The deal included the development of luxury tourist resorts in the city, as well as a port, a free zone, and a yacht marina. The government announced that it would invest about $150 billion over ten years, with the government receiving 35% of the profits, indicating that the government would participate in the investment through the construction of roads, water and electricity networks, etc. However, the exact nature of the partnership is not known, due to the lack of transparency about the deal and its details.

What distinguishes the recent Ras al-Hikma deal, besides the large size of the bailout, is the payment structure. Real estate development deals usually have such longer duration payment structures, with the price of the land or usufruct right paid in installments that may extend until the end of the project’s development. But during this deal, the government announced that the payment would be made in just two months, suggesting that an important part of the deal was the financial rescue of the Egyptian economy. On 6 March 2024, just two weeks after the deal was signed, the government devalued the Egyptian pound by 38% to a historic low of 50 pounds per dollar immediately after the devaluation. This deal or financial bailout prompted international institutions to offer another bailout package for the Egyptian economy. The IMF increased the value of the loan it had previously approved in early 2023 for the government, from $3 billion to $8 billion. The World Bank also announced a new financing package for Egypt worth $6 billion over three years, of which $3 billion would be allocated to support the government and $3 billion to the private sector. The EU then announced the signing of agreements with Egypt, including a €7.4 billion (US$8.06 billion) financing package over four years including loans, investments, and cooperation on migration to Europe and counter-terrorism. The pledges of $57 billion in dollar inflows came in just over a month after the Ras al-Hikma deal was signed, supporting the notion that Egypt needed a quick financial rescue.

The financial bailout was also a political bailout for the regime in Egypt. The crisis could not have lasted long before it produced great social anger, especially in light of the government’s inability to control inflation, especially in food prices. The IMF’s critical language and demands for structural reforms suddenly changed after the deal, and it suddenly rushed to conduct two reviews that had been delayed by nearly 10 months in order to disburse the second tranche of the loan to Egypt. The European Union and the Gulf itself, represented by the UAE and expectations of future deals from Saudi Arabia and Qatar, seemed more open to the idea of a financial bailout for Egypt.

Egypt has been subjected to many additional economic pressures as a result of the Israel-Gaza war, perhaps the most important of which is the continued decline in Suez Canal revenues due to the war and Houthi attacks on ships. But these economic pressures do not explain the rush for the large support packages; while they have been present since October 2023, the bailout did not materialize until after the Ras al-Hikma deal.

This brings us back to the geopolitical and political changes in the region resulting from the October 7 attack on Israel and the realized and potential consequences of the Israel-Gaza war, including the displacement of Palestinians in Gaza. Egypt became the last hope for stability and preserving the previously agreed-upon relationship with Israel, most importantly the Gulf normalization processes that had been ongoing since Trump’s term as president in 2016.

In the end, the Gulf support came in the form of a direct investment, through which the Abu Dhabi Fund acquired a large piece of land on the Mediterranean coast. The acreage provides the UAE with an important foothold on the Mediterranean coast, a free zone, and a port whose future uses are unknown. The deal is also expected to accelerate the sale of other Egyptian assets, whether real estate assets such as land and historic buildings, as in the Ras al-Hikma and hotel deals, or other types of assets that fall within the requirements of the asset sale program announced by the government last year.

The Ras al-Hikma deal illustrates the nature of the connections mentioned earlier between the real estate sectors in the Gulf, specifically the UAE, and the real estate sector in Egypt. Emirati private and governmental companies view Egypt’s real estate sector positively, due to the large volume of demand that is constantly renewed due to Egytp’s demographic growth. The prevailing culture of investing in real estate and the ability of remittances from Egyptians working abroad to finance a renewed demand for real estate also play an important role.

This organic link between the real estate sector in Egypt and the Gulf can be seen in coastal projects and in Cairo, according to a study conducted by Al Omran Observatory, which showed that Emirati investors own about 16% of the land portfolio in Cairo for listed companies and that Emirati and Saudi companies are heavily deployed in coastal projects, especially on the north coast.

Changes in Gulf Support

The Ras al-Hikma deal, along with the ongoing acquisitions since 2022 of some productive assets owned by the Egyptian government, has raised questions – especially among the Egyptian public, the political opposition, and others interested in the political economy of the region – about the changes in the nature of Gulf political and economic support for Egypt since 2013. Some of these questions have been accompanied by official statements, such as the Saudi finance minister, declaring that the era of unconditional aid is over. Many writers close to the Saudi crown prince have focused on criticizing the Egyptian army and the nature of its economic interventions. A number of Egyptian analysts believe that the expected Gulf support for Egypt should have come more quickly and should not have included asset purchases, especially since many of these asset purchases were made under the logic of commercial negotiations about gains and profits, instead of simply providing aid (as when the Gulf provided much aid to Egypt after 2013). Based on the data from the Gulf aid database compiled from news published by the International Institute for Strategic Studies, the Gulf has stopped providing aid through petroleum and petroleum products since about 2017.

The following table shows the estimated amounts of aid from 2012 to 2017, which amounted to about $6.4 billion. This aid does not cover a large percentage of Egypt’s oil and gas needs over the five years; most of it was concentrated in 2013 and had a major impact on the continued operation of important sectors after 2013, most notably the electricity sector, which suffered a major crisis before 2013 due to various causes including the lack of fuel. However, the Gulf has not shown a current willingness to give such petroleum grants to Egypt, despite the electricity crisis that is largely attributed to the lack of hard currency needed to buy fuel.

Table 2: Gulf aid in the form of petroleum products

| Year |

Month |

Country |

Amount (USD millions) |

| 2012 |

May |

Saudi Arabia |

$250 |

| 2013 |

|

Kuwait |

$1,260 |

| 2013 |

July |

Kuwait |

$200 |

| 2013 |

August |

Qatar |

$410 |

| 2013 |

September |

Qatar |

$410 |

| 2013 |

August |

Saudi Arabia |

$400 |

| 2013 |

September |

Kuwait |

$280 |

| 2013 |

September |

Saudi Arabia |

$400 |

| 2013 |

|

UAE |

$957 |

| 2017 |

|

Saudi Arabia |

$700 |

Source: Gulf Aid Database to Egypt – International Center for Strategic Studies

The Gulf stopped providing this form of petroleum support but continued to provide another form of support: deposits with the CBE. Gulf deposits represent about $29 billion, which is about 83% of the total foreign exchange reserves at the CBE estimated at $34.9 billion. They are divided between long-term deposits of about $15 billion renewed by the UAE, Saudi Arabia, and Kuwait since 2013, and short-term deposits (less than a year) of about $14 billion by these countries as part of the agreement with the IMF on the current financial rescue program. Short-term deposits represent about half of the short-term debt, an important change in Gulf support policy. In the past, the Gulf provided long-term deposits, maturing after three or five years. However, it seems that the main objective of the CBE giving short-term deposits is to put more pressure on the regime to undertake economic reforms, which may include removing the military from the economy and opening the private sector, demands that the IMF has long emphasized are within the scope of the structural reform plan to be pursued by the Egyptian government. The following table shows the movement of Gulf deposits to the CBE from 2012 to 2022.

Table 3: Movement of Gulf deposits to the CBE from 2012 to 2022

| Year |

Month |

Country |

Deposits (USD million) |

| 2012 |

August |

Qatar |

$2,000 |

| 2012 |

May |

Saudi Arabia |

$1,000 |

| 2013 |

May |

Qatar |

$3,000 |

| 2013 |

September |

Kuwait |

$2,000 |

| 2013 |

September |

Saudi Arabia |

$2,000 |

| 2013 |

July |

UAE |

$2,000 |

| 2013 |

July |

UAE |

$1,000 |

| 2015 |

April |

Kuwait |

$2,000 |

| 2015 |

April |

Saudi Arabia |

$2,000 |

| 2015 |

May |

UAE |

$2,000 |

| 2016 |

September |

Saudi Arabia |

$2,000 |

| 2016 |

August |

UAE |

$1,000 |

| 2017 |

May |

Saudi Arabia |

$1,000 |

| 2021 |

October |

Saudi Arabia |

$3,000 |

| 2021 |

October |

Saudi Arabia |

$2,300 |

| 2022 |

May |

Saudi Arabia |

$5,000 |

| 2022 |

May |

UAE |

$5,000 |

| 2022 |

May |

Qatar |

$3,000 |

| 2022 |

November |

Qatar |

$1,000 |

| 2022 |

November |

Saudi Arabia |

$5,000 |

Source: International Center for Strategic Studies, Gulf Aid to Egypt Database

The absence of Qatari deposits from 2013 until 2022 was due to the tension in relations between the Gulf in general and Egypt in particular with Qatar. However, Qatari investments and deposits gradually returned after the Gulf reconciliation in 2021. In that period, Egypt’s allies – including Saudi Arabia, the UAE, and Kuwait – continued to provide deposits to the CBE. Although deposits cannot be considered direct forms of support like petroleum grants, they play an important role as their interest rate is lower. If they are pegged for long periods, they act as a buffer against exchange rate depreciations and give the CBE the ability to act to support the currency in times of crisis.

The above data demonstrates that the nature of Gulf support has changed, not only through the nature of political statements and rhetoric between Egypt and its Gulf partners and the Egyptian position but also through the change in support itself. Since 2013, the Gulf stopped providing oil as grants to Egypt after the energy crisis had passed relatively quickly and later stopped providing long-term deposits; even when the current economic crisis erupted, it provided short-term deposits.

The commercial interests of the Gulf, specifically the Gulf sovereign wealth funds, have become an important factor in determining the amount and type of support to Egypt; this can be seen in the current Egyptian asset purchase program, which is linked to political arrangements between Egypt, the Gulf, and the IMF. But it is also linked to the nature of the assets the Gulf is acquiring in Egypt. Gulf support has become more conditional and linked to the Gulf countries’ economic and commercial interests. This does not completely negate the political nature of these acquisitions, but it makes it imperative to place these Saudi and Emirati acquisitions in a broader scope away from political support. Saudi Arabia and the UAE have not stopped directly supporting the regime through deposits in the CBE, which are provided without economic preconditions, unlike IMF loans, and at low interest rates.

Acquisitions of Egyptian assets are not new, and the Gulf has been one of the largest foreign investors in the Egyptian market. The total capital flows from the Gulf to Egypt since the beginning of the millennium constitute about $90 billion. Foreign investments from the EU are the second highest, at about $48 billion, followed by China with about $29 billion during the same period.

What Does the Gulf Hope to Gain from These Acquisitions?

The Gulf – if we can consider it as a single bloc – is going through a phase of profound transformations: the Arab Spring and its aftermath, the Iranian nuclear deal, and so-called the end of the oil boom that had lasted from 2000 to 2014. During that period, oil prices were continuously rising (except for the period of the global financial crisis in 2008), and with the consolidation of financial globalization, the Gulf entered into extensive processes of financialization and gained a more solid footing in the wake of that globalization due to its accumulation of financial surpluses from the increased Chinese demand for oil. The process of investing these surpluses changed in the period following the 2008 financial crisis: after the crisis, Gulf sovereign funds became more diversified in the assets they invested in, and their investment strategies diversified to become more focused on creating long-term surpluses, rather than investing in safer financial instruments such as treasury bonds of major countries, led by the US.

Different parties in the Gulf are trying to establish themselves globally through these political, economic, and social shifts. For example, the Sino-American rivalry over Africa represents an opportunity for the Gulf states to become involved and play important roles. This can be seen most prominently in the UAE’s interest in controlling ports in the MENA region. Saudi Arabia is using oil as a powerful weapon in trying to build foreign policy autonomy, particularly in the context of the Russia-Ukraine war; it is trying to replace the Iranian enmity with a more manageable rivalry, especially as its military objectives in the Yemen war have failed. Qatar, the third player in the Gulf, is trying to capitalize on its European and American relationships to prevent it from being swallowed up by rival Gulf powers.

These changes have grown the importance of the Gulf sovereign wealth funds; their objectives have expanded to include taking on roles previously performed by Gulf private sector companies in Egypt through direct investments. In the UAE, Saudi Arabia, and Qatar (the largest GCC countries in terms of aid and overseas investments), a pattern of large private-sector relationships can be observed, much like the patronage networks between businessmen and politicians in the global south. In the Gulf, sovereign wealth funds and government institutions hold large stakes in major private sector companies. Successive waves of privatization in countries such as the UAE have been aimed at involving the private sector in the management of the economy, rather than completely ignoring it, which largely ensures the distribution of surplus wealth produced by the oil and gas sectors, as well as sectors associated with the investment of those surpluses, especially the financial sector.

GCC sovereign funds are present in the ownership of local private sector companies in three main sectors. The first is the industrial sector, which focuses on energy-intensive and high-tech industries, such as petrochemicals, iron and steel, aluminum, and others. The second sector is infrastructure investments – on which Gulf countries are spending substantially – from real estate basic services such as telecommunications, water, and retail. The third is the financial sector, which is largely controlled by families that are either directly linked to the ruling families or directly controlling banks through investment funds in tax havens owned by princes and sheikhs from the ruling families. In the case of the Gulf, the large private sector cannot be separated from the state, as wealthy and corporate families are closely linked to the state, and the pattern of doing business is still family-oriented. Despite the internal governance of these family businesses, they still lack certain capitalist components of governance because they are linked to the power dynamics between the private sector and the ruling families. This close relationship between the state and capital in the Gulf can be understood by looking at all major economic sectors. The banking sector provides a clear illustration of this relationship, with all large banks in the GCC having a mix of ownership between public investment funds, ruling families, and large private sector trading companies.

The importance of Egypt to the Gulf can be summarized in a number of reasons related to the similarity of the economic structure, market nature, and business culture between the Gulf and Egypt. Egypt’s position can be understood as suitable for the Gulf’s economic diversification and its search for what can be called the expansion of the geographical reach of the Gulf capital. Egypt represents a suitable ground for the economic diversification of Gulf capitalism and its expansion in the region because it has the large market needed for mass sales of final consumption products. The lack of purchasing power in Egypt is compensated by a large number of people capable of consuming, which explains the Gulf's interest in the food and retail sector, and other sectors such as real estate. Large real estate companies, such as Emaar and Aldar Properties, have created the conditions and ingredients needed for real estate expansion in Egypt. Gated communities have been built in Egypt in the desert, as in Dubai, Riyadh, and other Gulf cities. By partnering with the Egyptian private sector, these companies have been able to reshape the urban environment in Cairo’s desert suburbs and in Egypt’s coastal cities in the style of Gulf urbanism. Geographical proximity and ease of trade also play an important role in stimulating investments between the countries, thereby facilitating capital flows from the Gulf into Egypt. Over the last ten years, for example, the destination of Egyptian agricultural exports has shifted significantly toward the UAE and Saudi Arabia, whose companies in Egypt’s agricultural and food sector became more present after 2008.

But perhaps the most important driver behind the Gulf flows into Egypt, especially the flows between the private sector in the Gulf and Egypt over the past decades, is the similar nature of the private sectors in Egypt and the Gulf. For example, patronage relations between the regime and the private sector are similar, although, in the case of Egypt, they take more subtle forms due to the nature of the republican political system. The levels of concentration are also very similar. In Egypt, the banking sector represents a large weight of listed companies, similar to the major Gulf stock exchanges. The levels of concentration in the banking sector in the Gulf are also similar to Egypt in terms of deposits or otherwise. In Egypt, the government owns the banks directly, while in the Gulf they are owned through alliances between the private sector and the government. In all economic sectors, similar concentrations can be found between Egypt and the Gulf, which can be attributed to the generally weak antitrust regulatory and supervisory structure in the region. But even such high levels of economic concentration can be observed in countries with better market regulation.

GCC investments in Egypt, as in the recent wave of acquisitions, also illuminate the competition between Saudi Arabia and the UAE for Egyptian market share, with the UAE, with a smaller population and a smaller market, being more interested in the Egyptian market.

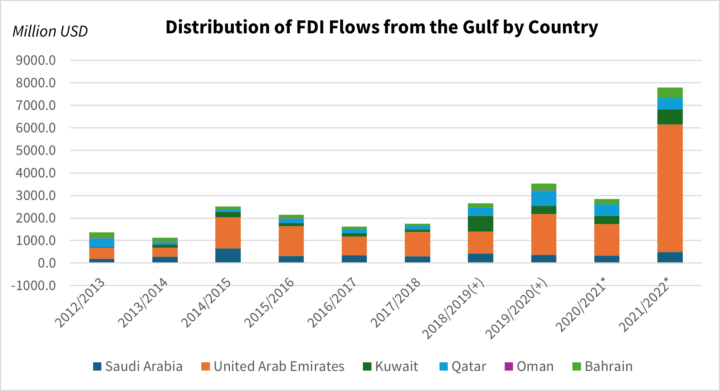

The following figure shows the distribution of Gulf direct investments in Egypt over the past decade.

The expansion of Gulf capital into Egypt and other countries in the region has been driven by the intense financialization of Gulf economies, particularly since the turn of the millennium. As financialization took place, the banking and non-banking financial sectors rose in Egypt as well as in the Gulf. This is characteristic of the financialization processes in developing and southern countries that has been largely initiated by international institutions, such as the World Bank and the IMF. However, the Gulf countries have engaged in the global financial system from a position of relative strength due to their large oil revenues, which is reflected in the types of trade and their proportion to the GDP in the Gulf countries. The extensive use of migrant labor has also increased the interconnectedness of Gulf economies with other economies in the region. Egypt joined the wave of financialization less aggressively, seeking to borrow either through international debt markets or regional debt markets in the Gulf as the only option available to it due to its absence of oil surpluses. However, its increase in regional connectivity was driven by remittances, which played an important role in the capital formation of many sectors, most importantly real estate with its renewed demand largely financed by remittances. Thus, remittances from Egyptian workers and Gulf capital played an important role in linking the Egyptian economy to the Gulf economies.

Economic diversification was not the only goal of Gulf investments. The Gulf may have become more interested in commercial interests and economic diversification over the past years, but this cannot explain the Gulf deposits in the CBE and its support in the form of gas and oil shipments. Thus, one of the goals of the Gulf’s attempt to support Egypt is to achieve economic and political stability, supporting the political regime to finance the budget and maintain a stable – even if nominal – exchange rate and a consequently greater ability to control inflation. However, the search for economic stability may have become limited over the past years, especially since the Gulf support did not result in structural reforms such as improved governance of government spending, according to the Gulf and the IMF; indeed, heavy investment in infrastructure projects through foreign borrowing instead resulted in the current debt crisis.

Gulf investments and deposits in Egypt also contributed to the consolidation of the Gulf’s political and geopolitical hegemony over the region, specifically in the context of the rivalry between Saudi Arabia, the UAE, and Qatar for regional leadership. This rivalry had emerged before the boycott of Qatar but after the reconciliation and the outcome of the war in Yemen, in which Saudi Arabia and the UAE supported different parties and had disparate objectives. The current Saudi–Emirati rivalry can also be seen in Saudi Arabia’s attempt to diversify and modernize its economy to move away from oil, and the consequent competition between Riyadh, Dubai, and Abu Dhabi to be the financial and entertainment center in the region. Geopolitical hegemony over Egypt is also a very important goal for any political project in the region. Egypt has historical and cultural weight and extensive relations with traditional Gulf allies such as the US, and allies with whom the Gulf wants to strengthen ties such as Israel and Russia. Its geographic location on trade routes between China and Europe is essential for cross-border trade projects that have become increasingly important over the past two decades: consider China’s Belt and Road Initiative and the US reward announced in September 2023 for the India-Middle East-Europe Economic Corridor.

Conclusion

The recent Gulf acquisitions can be seen as a link in a chain of a series of attempts by Gulf wealth funds to diversify their investments in the region and increase their effectiveness in controlling sectors in which they are already present, expanding the scope of Gulf capital. This latest wave of Egyptian acquisitions came against the backdrop of a severe economic crisis, and many believed that it carried too many conditions compared to other forms of support that the Gulf had previously provided. Of course, the wave of acquisitions carried conditionalities that partially disrupted the supposed financial bailout of Egypt. But these conditionalities, primarily related to the commercial and economic interests of Gulf companies, were always present and an important part of the equation of the interaction between Gulf capital and Egypt.

The Gulf continued to provide deposits to the CBE, and deposits of shorter duration, to pressure Egypt to adopt the set of policies desired by the Gulf and the IMF, which seems to have been more insistent in the latest loan agreement that the Gulf take greater responsibility for bailing out Egypt’s financial situation. There is a change in the nature of Gulf support for Egypt, but it is part of the Gulf’s changing priorities in the region and the world, and the Gulf’s positioning itself in recent years as part of the global financial sector. In a sense, this shift would have happened whether or not Egypt succeeded in its economic reforms since 2014, because Gulf sovereign wealth funds have become more important in the diversification and internationalization of Gulf capital over the past decade.

What characterizes this ongoing cycle of acquisitions is not only its complex political and commercial nature but also the fact that it represents one of the links between the Egyptian economy and the Gulf economy. Not only is the Gulf looking for a way to invest its financial surpluses, but it has completely changed the nature of the region’s political economy, with most of Egypt’s major economic sectors now tied to the Gulf. The organic link in economic value creation between Egypt and the Gulf now forms a different loop than before: remittances from workers abroad, which used to be the most important part, are joined by investments and acquisitions. This can be seen as part of the Gulf funds’ diversification of their investments in the region, but it is also part of the reorganization of the region’s political economy so that the Gulf, especially the states with political projects such as Saudi Arabia, the UAE, and Qatar, are effectively in control of the region’s most populous countries.

What this paper tries to emphasize in the end is that the change in the nature of Gulf support was directly related to the political and economic changes within the Gulf and the Gulf funds’ attempt to establish an economic hegemony in the region, especially in the strategic sectors in which Gulf companies have experience: energy-intensive industries; the sectors that shape the urban environment including the real estate sector, telecommunications, and other basic services; and the financial sector, both banking and non-banking, which ensures the investment and reinvestment of those Gulf surpluses outside the Gulf.

The views represented in this paper are those of the author(s) and do not necessarily reflect the views of the Arab Reform Initiative, its staff, or its board.