Abstract

In October 2019, an already strained economy in Lebanon suffered a sapping shock that led to a palpable shortage of US dollars, limitations on foreign currency withdrawals and transfers, substantial devaluation of the Lebanese currency, and massive loss of purchasing power. The economic downfall had a crippling effect on all healthcare sectors including hospitals, healthcare providers, and the pharmaceutical and medical supplies industry. The outbreak of COVID-19 further aggravated the crisis. To address the health care crisis, Lebanon needs a dual tracked plan, with immediate measures to tackle the short-term urgency and a medium/long-term effort to address the health sector’s structural issues. In this paper, we present some essential reforms needed in the short-term. The approach focuses on maintaining access to healthcare for all, enhancing primary and urgent care centers, controlling readmission [subsequent admission of a patient within a month for the same health problem], and introducing telemedicine. Immediate measures will be needed to reduce the financial strain on hospitals, as well as hospitalization costs. In parallel, efforts are needed to support healthcare providers and address the challenges facing the pharmaceutical and medical supplies industry. These efforts can include direct and indirect monetary support, along with guiding principles to support the people behind these industries while maintaining the quality of the products and services they are providing.

Introduction

October 2019 was a turning point in Lebanon as the country suffered from an economic shock with downstream effects that shattered every sector. After banks closed for several weeks, the Lebanese public came to discover that foreign currency reserves in the banks and the central bank were depleted and that depositors suffered from arbitrary capital control measures unsanctioned by official authorities. The Lebanese market suddenly experienced a palpable shortage of US dollars, leading to multiple parallel exchange rates exceeding the official rate, severe limitations on dollar withdrawals, and harsh restrictions on international transfers of foreign currency from the country (Harake & Abou Hamde, 2019). The outbreak of COVID-19 in February 2020 further aggravated the economic turmoil, with the whole country going into lockdown for nearly six weeks. In a country that is highly dependent on tourism and services, COVID-19 weighed heavily on an already strained economy that was suffering from high inflation and unemployment rates (Central Administration of Statistics, 2020), a greatly negative balance of payment, and high public debt (The World Bank, 2020b).

Similar to other countries, Lebanon’s supply chain of goods, including medical supplies, was deeply impacted by the pandemic. However, while many other countries have managed to cushion the impact of COVID-19, Lebanon has thus far been incapable of doing so as it struggles with a severe financial crisis and an unprecedented economic depression. The World Bank expects a prolonged crisis, further loss of purchasing power, and spikes in poverty and unemployment rates (The World Bank, 2020a).

This paper examines the effects of multiple economic strains on the healthcare system with specific focus on the hospital sector, healthcare providers, and the pharmaceutical and medical supplies sector. As with other economic sectors in Lebanon, the healthcare sector is facing significant challenges that cannot be overcome unless serious reforms are implemented. Immediate and long-term plans for reform are needed. This paper focuses mainly on the immediate short-term actions/solutions needed to prevent a total collapse of the healthcare system and ensure the solvency of individuals and families in need of medical care. This is of major importance in light of the recent announcement by Lebanon’s central bank (Banque Du Liban, BDL) that all subsidies, including those to medications and medical supplies, shall be suspended by November 2020.

Overview of the Lebanese Healthcare System

Over the last two decades and in the aftermath of a devastating civil war (1975-1990), the Ministry of Public Health (MOPH) has taken many steps to strengthen the health system and ensure better quality and access (Wim Van Lerberghe, 2018). Lebanon ranked 33rd among the 195 countries in the Healthcare Access and Quality (HAQ) index in 2018 (Fullman et al., 2018). It ranked first among all the Middle East countries and recorded the best performance among high-middle socio-demographic index (SDI) countries in terms of the HAQ index, along with Saudi Arabia and Turkey. Moreover, Lebanon’s life expectancy at birth is 76.28 years - the third highest in the Middle East after the UAE and Qatar. It has also succeeded in significantly lowering infant mortality rate, neonatal mortality rate, and under-five mortality rate over the last 30 years (World Health Organization, 2020).

Healthcare delivery for inpatient treatments is undertaken by a network of private and public hospitals. According to the MOPH website, public hospitals account for 18% of the total hospital beds in the country (Wim Van Lerberghe, 2018). Private clinics are utilized the most for ambulatory services. In addition, an expanded network of primary health care centres and dispensaries run by the MOPH and charitable organizations cater to lower-income segments of the population who cannot afford private ambulatory care.

While the prices of medications are subject to pricing structures set by the MOPH, many medications remain unaffordable for low-income patients. Through the primary health care centers network, the MOPH, in collaboration with the YMCA and other NGOs, dispenses essential medications for chronic diseases free of charge (Wim Van Lerberghe, 2018). There are 650 active dispensaries distributed across all governorates (Epidemiological Surveillance Program, 2015), alongside 238 primary healthcare centers (Lebanese Ministry of Public Health). The MOPH has sought to enhance the quality of care provided by ensuring that these centers can offer a basic set of health services and products that are financially supported for everyone (known as the Essential Healthcare Package) , and by introducing an accreditation system that sets the quality standards and prompt continuous improvement in these centers to implement (Hemadeh, Hammoud, & Kdouh, 2019; The World Bank, 2020a).

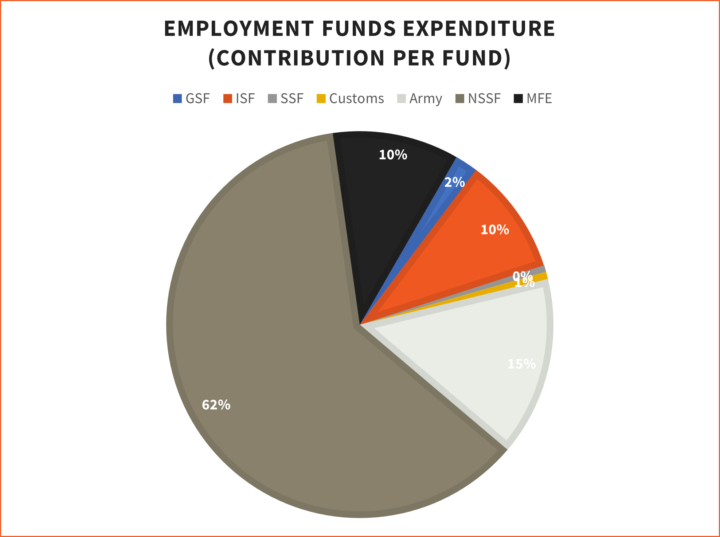

In 2017, the government, through the MOPH and military funds that cover the Lebanese army and their families, financed 21.4% of the cost of healthcare goods and services spent in the country (known as Current Health Expenditure, [CHE]). Funds based on employer contributions (excluding the military as an employer) such as “The National Social Security Fund” and the “Civil Servant Cooperative” covered 23%. While private insurance companies covered 19.1%, NGOs covered 3.1%. the rest are out-of-pocket (OOP) accounting for 33.1% of the healthcare expenditure (Lebanese Ministry of Public Health, 2006-2018). Nonmilitary employer-based healthcare coverage funds are publicly managed in Lebanon and include:

- The National Social Security Fund (NSSF), a fund based on contributions by employers for employees of the private sector. To note: Home care is not covered by the NSSF. In 2018 26% of all citizens benefited from the NSSF (Statistics, 2019).

- The civil servant cooperative covers civil servants. 3% of citizens benefited from the civil servant cooperative in 2018 (Statistics, 2019).

The distribution of their contribution to the total expenditure by employment (both military and nonmilitary) funds is shown in figure 1(Lebanese Ministry of Public Health, 2006-2018) with the NSSF contribution accounting for most of the employer-paid health expenditure.

Figure 1 - Distribution of the employment funds’ expenditures among the different agencies.

Key: GSF: General Security Forces, ISF: Internal Security Forces. SSF: State Security Forces. NSSF: National Social Security Fund. MFE: Mutuelle des Fonctionnaires de L’état (Civil Servant Cooperative)

People who do not qualify to benefit from the employment funds and who do not have the means to obtain private health insurance are in principle covered by MOPH (Ammar, 2003). In addition, since 2016, all Lebanese senior citizens (65 years and above) are in principle covered by the MOPH for hospitalizations ("Decree number 109 by MOPH, Change in Proportion of Health Coverage," 2016).

In 2012, only 8% of those eligible for MOPH coverage utilized that coverage (Lebanese Ministry of Public Health, 2006-2018). There has also been discontent among many Lebanese about their lack of access to hospitalization coverage, despite the structure mentioned above ostensibly having them covered. This could imply the exclusion of many from the coverage of the MOPH, contrary to what is on paper. Politics, confessionalism, and religious affiliation have affected access to healthcare in Lebanon (Chen & Cammett, 2012; Khalife et al., 2017), and it is reasonable to expect that access to MOPH coverage is also affected by these same factors. With rising unemployment rates, more citizens will no longer qualify for employment funds and will rely on the MOPH or OOP expenditures to cover their health expenses, all while being unable to pay for private insurance premiums as their purchasing power keeps decreasing.

The NSSF has been recording a budget deficit for several years, and some hospitals have been turning down MOPH covered patients since the ministry is failing to pay for those who theoretically qualify for coverage (Mikhael, 2018). Since the NSSF is the largest contributor among the employment funds and the MOPH is the final safety net for citizens with no coverage, their failure to meet obligations significantly affects the goal of universal healthcare coverage. The MOPH’s budget, has witnessed a significant increase from USD 232.945 million in 2005 to USD 485.899 million in 2018 (assuming the official exchange rate of 1500 LBP/USD) (Lebanese Ministry of Public Health, 2006-2018). The highest amounts spent by the MOPH are for hospital bills and medications accounting for 64% and 22% respectively in 2018.

Over the past 15 years, Lebanon’s health expenditures increased by 57% to reach USD 719 per capita in 2017. As a percentage of its GDP, Lebanon has one of the highest health expenditures among Arab countries (8.20% in 2018) (The World Bank, 2020b). Even though the Lebanese healthcare system has achieved good quality standards (discussed above), high healthcare spending does not eliminate disparities in access nor does it ensure safety from catastrophic expenditure for the poor (Salti, Chaaban, & Raad, 2010).

Conditions of private hospitals

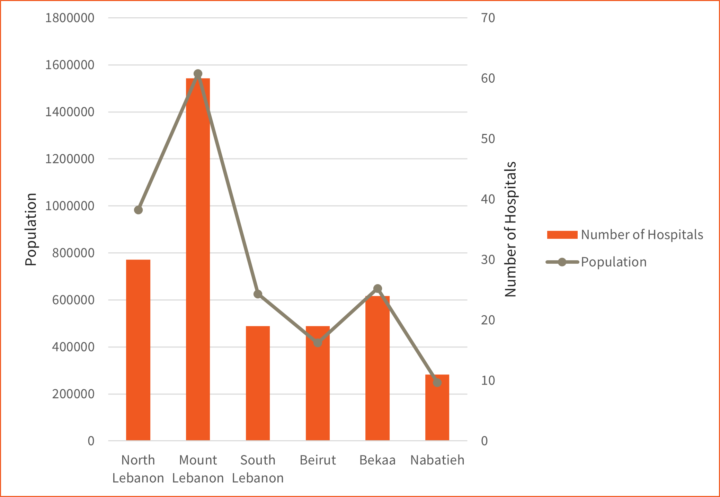

The latest economic turmoil in the country has severely hit hospitals. There are 163 hospitals in Lebanon (figure 2) (Health, 2020; Lebanese Ministry of Public Health, 2006-2018). To date (September 2020), hospitals are still billing for services at the same prices when the official exchange rate was 1500 LBP/USD compared to the current black-market exchange rate that is closer to 8000 LBP/USD.

Moreover, due to the financial challenges faced by insurance companies, many of them are issuing policies that exclude major hospitals - the more expensive ones - in order to provide lower and more affordable premiums (Schellen, 2018). In addition, the diminishing purchasing power of families is preventing many from buying private insurance policies (Middle East Insurance Review, 2020). The lack of insurance coverage for many has led to a decrease in the patient load in major hospitals (that usually charge higher prices). These individuals and families are left with no other option but try to rely on the MOPH to cover their healthcare bill.

Historically, the MOPH and the NSSF have always been in debt to hospitals with delays in paying bills (Mikhael, 2018). These overdue bills are in LBP, and therefore are subject to all the impact of devaluation at the date of account settling. With the increase in the patients’ reliance on the MOPH, the losses incurred by NSSF, and the increase in the expenses of both entities, it would be even more difficult for both the MOPH and the NSSF to fulfil their obligations to hospitals, which would further affect hospital financing. While the government decided in November 2019 to subsidize certain elements of healthcare by supplying foreign currency at the 1500 exchange rate (such as medical supplies, and medications), other vital elements are not included in this subsidy scheme. For example, spare parts for medical equipment are not subsidized and maintenance contracts for medical equipment are often breached by the manufacturer. Consequently, to remain functional and minimize losses, many hospitals have resorted to decreasing employees’ wages, laying off some employees, furloughs, and downsizing or closing some services. Despite these painful cost-saving measures, the current situation is not sustainable; the head of the private hospital syndicate Sleiman Haroun reported that 15 hospitals are in imminent danger of closing and headed towards collapse (The Daily Star).

Figure 2. Number of hospitals per district plotted along with the population size of each district

Challenges to healthcare providers

Lebanon has an abundance of Physicians to cover its healthcare needs. There are 22.71 physicians for every 10,000 people, the fifth-highest density in the Eastern Mediterranean region. On the other hand, it suffers from a shortage of nurses, with 16.74 nurses and midwife personnel per 10,000 people, giving it a rank of 12/22 in the region (World Health Organization, 2020). All healthcare workers have been subject to immense pressures due to the economic and financial crisis. Medicine in Lebanon is categorized by law as a "liberal profession”, and thus physicians are regarded as independent professionals and can be self-employed. Accordingly, physicians are not salaried employees whether they work in private clinics or in large hospitals. Physicians’ income is generated from professional fees that are charged separately from hospital fees. In private clinics, physicians receive their professional fees directly from the patients. Similar to hospitals, physicians’ professional fees as set by the Order of Physicians are still based on LBP, with only minimal adjustments to address the new exchange rate to the USD or to the new inflation rate. This, added to the drop in the purchasing power in Lebanon and the drop in hospitalizations witnessed during the COVID-19 outbreak, has led to a significant decrease in physicians’ income. Similar to other countries, physicians' income has dropped by 50% because of COVID-19 (Fair Health, 2020). However, in Lebanon, as the drop was also accompanied by devaluation of the LBP (from 1500 to 7500), the total expected loss in purchasing power is more than 80%

For the same reasons, many nurses were subject to salary cuts, layoffs, or furloughs (Deeb, 2020). Accordingly, many physicians and nurses are contemplating leaving the country and securing better positions elsewhere. Since July 2020, more than 300 doctors have officially made requests to their hospitals and the order of physicians to leave to work abroad, and more than 200 nurses have done the same (Lewis, 2020).

The pharmaceutical and medical supplies sector

There are 2,614 pharmacies across Lebanon, with the majority concentrated in Mount Lebanon (Order of Pharmacists of Lebanon, 2020). According to the syndicate of pharmaceutical industries in Lebanon, the Lebanese pharmaceutical market totalled USD 1.98 billion in 2019, of which USD 139 million (7% of the total market) were for products manufactured locally (Al Akhbar).

Since October 2019, Lebanon’s central bank (BDL) has started subsidizing pharmaceutical products (including raw material for local industry) by providing 85% of the foreign currency needed for pharmaceutical imports at the previously utilized official exchange rate (Banque Du Liban). Along with the structure already in place for drug pricing, these measures were supposed to ensure a stable price for consumers and the continuity of business for importers and pharmacists. However, since June 2020, a shortage of medications was noted in the market. Besides the supply chain disruptions due to the COVID-19 outbreak, several local and potentially manageable factors also contributed to this shortage including: the smuggling of subsidized medications outside of the country, the stockpiling of medications by patients and local warehouses in anticipation of future pricing hikes, and the delayed processing time for subsidies by BDL (Elsunhawy; Hamiye). Another undeclared and contributing cause is the potential conflict in the pricing structures between importers and the MOPH.

At the level of distribution to patients, the Lebanese syndicate of pharmacies has reported the closure of 200 pharmacies so far, with another 800 at risk of closing down (Sawaya). The latter is because of significantly reduced profitability and losses incurred during the current year. Pharmacies in Lebanon sell pharmaceutical products like medications at a fixed profit margin that is set by the MOPH and based on the subsidized exchange rate. As the Lebanese pound depreciates, the actual value of the pharmacies’ fixed profit margin from the sale of medication has decreased. Pharmacies have also seen a drop in their sales of ancillary products as these have become more expensive. The net outcome is the bankruptcy of many pharmacies.

A similar subsidy policy governs the importing of medical supplies and medical implants into Lebanon, though medical equipment and maintenance parts are not covered. Thus, importing any new equipment is currently subject to securing foreign currency from the black market. As the current pricing of medical services delivered remains at their pre-October 2019 levels, health providers have little incentive to purchase any medical equipment currently.

Solutions moving forward

The influx of Syrian refugees during the past years had already imposed a heavy burden on the different pillars of the Lebanese healthcare system from primary healthcare centres to tertiary care (Dumit & Honein-AbouHaidar, 2019). The Lebanese healthcare sector is currently under the crushing impact of three economic factors in addition to that of the COVID-19 outbreak: 1. Loss of purchasing power of the patients; 2. Capital control measures; and 3. Devaluation of the Lebanese currency. While BDL did step in to mitigate the impact of the capital control measures on this particular sector, a more comprehensive plan is needed. This is an urgent matter, especially in view of the recent announcement by BDL that, by November 2020, it will halt all subsidies due to its depleted foreign reserves.

From the experiences of other countries, cutting healthcare spending as part of austerity measures has been shown to have serious negative consequences on public health (Quaglio, Karapiperis, Van Woensel, Arnold, & McDaid, 2013), and had an even greater impact on access to healthcare than the economic crises themselves (Stuckler, Reeves, Loopstra, Karanikolos, & McKee, 2017). As such, a response plan ought to be developed jointly between the MOPH, representatives of the various members of the health sectors, and representatives of other ministries involved. The goals of this plan should be to ensure accessible healthcare service and sustain the healthcare sector during the acute dip pending reaching a new steady state.

We provide one framework to approach the problem based on expense reduction with maintenance of healthcare quality along with financial solutions to keep the components of the healthcare sector operational.

Decreasing health expenditures and containing costs should not in any way compromise quality. With limited resources available and with the need to give the patient the best of what is available, strategies and policies must be put in place to facilitate the adoption of a patient-based and inter-organizational collaboration in the management of healthcare costs. This will bring together hospitals in the private and public sector, the MOPH, and patient advocacy groups to coordinate efforts, guide policy, and resource allocation for better healthcare services.

Although certain patient populations (the most vulnerable, patients with less grim prognoses, and sick healthcare workers…) should be prioritized, no patient should be left behind solely because of financial restraints. Therefore, any decision-making process should study the consequences of the decisions made, maximize the benefits to the person, and prioritize impartiality and the consequences towards the wider group of people affected by decisions (not just the individual) (Felzmann, 2017). Experience from countries that underwent similar changes is a clear indicator that such a process will help guide policymakers in tough decisions, alleviate their anxiety, and ensure transparency for the public (Brall, Schroder-Back, Porz, Tahzib, & Brand, 2019).

In a similar manner, efforts should be made towards measures that have the most potential to reduce costs incurred on patients and financing agencies. We propose some areas that could be good targets to reduce expenditure.

Enhancing primary and urgent care

Although primary healthcare centres by the MOPH are distributed across the country, they still remain underdeveloped with no provision of basic diagnostic imaging and laboratory medicine. Patients still have to seek care in hospitals should they require any diagnostic tests, especially in an emergency. Primary care centres can help increase access, improve health, control illness, and decrease costs by preventing excessive charges incurred by hospital bills, thus keeping hospitalization as a last resort for patients who objectively need it. The literature supports the cost-effectiveness of a switch to primary care. For instance, during the economic crisis after the fall of the Soviet Union, the Cuban healthcare system heavily relied on primary care local clinics. Even though secondary and tertiary care was severely impacted by the crisis, Cubans were very satisfied with their primary healthcare system (Nayeri & López-Pardo, 2005). Studies have shown that primary care and family medicine attributes do contribute to better health outcomes and to a decrease in cost along with less use of resources and hospitalization (Sans-Corrales et al., 2006). Thus, further investing in expanding the network of primary health care centres to the areas in need and studying which of them can be developed to provide urgent care with laboratory and imaging testing is an essential path. Exploring the possibility of linking these centres to neighbouring facilities (hospitals, diagnostic centres...) for testing and referrals is also needed. Shifting care from hospitalizations to primary care centres, along with preventing readmissions (discussed below) is important in conserving hospital resources to treat COVID-19 patients given that the number of COVID-19 hospitalizations is rising.

Preventing readmissions

A readmission is the hospitalization of a patient within a short period of time after discharge from an initial hospitalization for the same diagnosis, or as a consequence of that diagnosis. Readmissions add a large burden on patients from the points of view of both symptomatology and expenditure. In a large population study among different US states, the cost per year for patients who had a readmission was more than double that for patients without readmissions. In this study, the number of chronic medical conditions was most correlated with the readmission rate. Patients with heart failure also had the highest probability of readmission (Friedman & Basu, 2004). Taking the model of heart failure, establishing adequate outpatient care by heart failure clinics, prompting follow up with a primary care provider, and ensuring adequate patient education are among many interventions that can prevent heart failure readmission (McClintock, Mose, & Smith, 2014). Basing policy on these three areas can reduce readmissions and subsequently costs on government, patients and covering agencies.

Telemedicine

Despite some disadvantages, telemedicine - the remote diagnosis and treatment of patients by means of telecommunications technology - can help enhance healthcare for chronic illnesses. Efforts leading to guidelines and legal frameworks should be put in place to ensure the adequate protection of patients’ data, along with the necessitation of patients’ consent to parties that should have access to their records (Nielsen et al., 2020). In Lebanon, during the COVID-19 spread, the Lebanese Order of Physicians (LOP) issued a statement authorizing telemedicine. However, this statement lacks the regulatory framework to address numerous challenges including limitations, reimbursement, and the medico-legal aspects. Addressing these issues in coordination with the MOPH and the Lebanese Parliament in an expedited manner represents a good opportunity not only for local patients but also for patients with established care in Lebanon who used to come from neighbouring countries. Along with the ethical and legal aspects, public infrastructure should be addressed if telemedicine is to become a part of healthcare in Lebanon. With the power cuts and narrow data bandwidths, Lebanon lacks the proper infrastructure that is needed to support a reliable telemedicine service. Because of the lack of technology access among underserved areas, user-friendly mobile health applications can be implemented and have shown success in low-income countries worldwide (Barnes, 2020). Telemedicine can also be used for a remote assessment of COVID-19 symptoms in terms of need for testing or hospitalization while minimizing exposure of the community and healthcare workers.

Hospitalization cost reduction

A large part of the hospitalization costs in Lebanon is driven by medication (Abdo et al., 2018) and medical implants costs. The cost of medical implants in Lebanon is higher than other countries with similar economic position. Furthermore, BDL subsidizes 85% of medical implants, leaving 15% purchased at the black market exchange rate of 7500 LBP, meaning that if an item used to cost 100 USD (150.000 LBP at the official rate) it now is 240.000LBP (a total increase of 60% in LBP).

Reducing this cost can be modeled on successful stories in India, for example (Wadhera, Alexander, & Nallamothu, 2017). In the Indian experience, prices of certain medical implants were largely inflated. In response the government implemented pricing brackets which were primarily drawn from enhanced profit margins in the local market. No similar study has been conducted in Lebanon, but indicators (the high cost of medical implants compared to other countries) point to this problematic area. Similarly, drugs in Lebanon are imported with good quality criteria but from a business perspective, the present criteria do not allow for good bargaining power to reduce cost. For example, there are numerous generics for a single molecule of statin. Lebanon should negotiate to buy generics at better prices; the introduction of these better-priced generics into the market will force importers from other manufacturers to decrease their prices to better compete.

On another front, the minister of public health has publicly announced that certain hospitals’ bills were inflated (National News Agency). This indicates that the system currently in place to verify the decision to hospitalize and the treatment adopted needs to be strengthened in order to curb greedy profit and minimize fraud. Corruption and fraud can be evidenced by the inflation in healthcare bill and can be seen in the surplus in healthcare markets encouraging unindicated use, along with a lack of laws that permit practices of accountability, transparency, and access to information (Malak, Hassan, & Ferdous, 2020). The magnitude of the anticipated reduction in cost from combating fraud is not known in Lebanon. However, corruption in healthcare is a worldwide phenomenon; and experience from the United Nation’s Development Program (UNDP) (Kohler, 2011) office in Lebanon and U4-Anti-Corruption Resource (U4 Anticorruption Resource Center, 2020) can help in this domain. The important central idea when combating fraud is to understand that all entry points into the health care system need to be covered in a systematic manner in order to achieve results. The full extent of healthcare fraud in Lebanon, and for that matter in other countries, cannot be measured precisely. Any successful effort to stop fraud and abuse without unduly burdening legitimate providers, requires aggressive, innovative, and sustained attention to protect all stakeholders, including patients, hospitals, and providers.

Monetary and financial solutions for hospitals

The monetary crisis impacting Lebanon is without a doubt the primary driver of numerous recent challenges. The sustainability of hospitals in this critical period, especially with COVID-19, is paramount. Hospitals are being asked to create and expand COVID-19 units. The measures we will describe can help hospitals in the process of equipping these units with supplies and personnel. A general overview of hospitals’ challenges listed above points to the problems. The budgets of hospitals consist primarily of employees’ wages, medical and pharmaceutical supplies, other supplies, and capital investment. While employees’ wages are still in LBP and have already depreciated with the currency devaluation, hospitals have further reduced their wage bill with cuts, layoffs, or furloughs.

The other element requiring attention is the change in the currency exchange rate, which is driving the cost upward depending on how much each item is subsidized. However, three considerations need to be attended to in this system. First, Lebanon has been the destination for many patients from all around the Arab region seeking healthcare (in what is known as ‘health tourism’); as such, many of the patients are non-Lebanese coming to Lebanon for healthcare. These patients are capable of paying according to a different scale for medical implants and other expensive items. Therefore, non-Lebanese should be treated as per a different scale. This applies to medical tourists who have available funds to cover their healthcare, with exceptions made regarding refugees who are mostly covered by NGOs. Second, the subsidy system has no evaluation and monitoring arm ensuring that there is no smuggling or overuse of items. Third, there should be some form of monitoring on what brands are being subsidized, as a failing economy should focus on subsidizing the cheapest yet effective medicines and not necessarily pay a premium for particular brands when cheaper alternatives are available.

Another solution that may be considered for alleviating the monetary problems would be to provide loans for hospitals at very low rates. These loans could be used to cover for operational expenses including, maintenance of medical equipment. Other solutions can come from looking into the list of variable costs that hospitals incur (electricity bills, for instance) and studying what steps can be taken on this level.

Finally, it is obvious that the above solutions cannot run for a very long time and therefore there should be a cap period of one year for revisiting the above. These solutions should be seen as a sector stabilizing package and can be ideally tied with some strings to ensure that no further layoffs happen. It must be clear to everybody that these are mostly transitional until the COVID-19 crisis wave has passed and that they are only in effect pending macro-solutions for the country’s monetary and financial structural problems.

Support for healthcare providers

Adjustments to assist healthcare providers need to happen as well. In July 2020, the Lebanese Order of Physicians (LOP) initiated an increase in the outpatient visit fee by 30% (El Nashra) and a request to the governmental insurance agencies and private insurance agencies to increase the basic fee physicians are reimbursed for in procedures based on the black-market USD exchange rate. This adjustment came after the LOP considered resetting all fees based on the electronic exchange price platform which is the most commonly used to determine the black-market exchange rate in Lebanon nowadays. Had the second option been implemented, it would have led to a higher adjustment that would have been perceived as a significantly higher barrier to access health care. The physicians’ order has pledged to revisit the whole scheme quarterly.

Nurses’ wage, on the other hand, are subject to existing labor contract terms and therefore suffer from a negotiation disadvantage. Although the Order of Nurses in Lebanon issues a salary scale every 3 years, with the last one issued in April 2018, most hospitals have yet to comply with it given their dire financial situation. There is a need to amend the law governing the nursing profession by the parliament to allow the Order, in coordination with the MOPH, to compel the salary scale on hospitals and employers. Another measure is to ensure that nurses remain employed through a variety of steps, including linking monetary support to hospitals with a cessation of layoffs. Ensuring that nurses remain employed also ensures they and their families have health insurance coverage from the National Social Security Fund. Furthermore, as we are living during COVID-19, many nurses are becoming either infected or exposed and are therefore requested to remain in quarantine. Thus, working through the above scheme guarantees that hospitals do not lose the human resources needed to continue their battle against COVID-19. Salary scale adjustments could be commenced once the situation becomes more predictable for hospitals.

Pharmaceutical industry

The local pharmaceutical industry production accounts for less than 10% of the market share (Al Akhbar). The industry is currently working at 50% of its capacity, according to the syndicate. Currently, medical supply and pharmaceutical imports are tax-exempt and are only subject to a customs fees rate of 5% (Lebanese Customs Administration, 2020). This has helped the availability of a wide range of medications at lower prices, but has left local production at a disadvantage. Unlike the situation of other countries, there are no pharmaceutical trade policies that give the Lebanese industry an advantage in exports. For example, Jordan and Egypt have increased their pharmaceutical exports by benefiting from free trade agreements with many countries (AMWAL Invest, 2010; Mohamed, 2018). A plan for the industry to increase its market share is highly needed, with clear short term targets to address the pressing needs of Lebanese patients, and longer-term targets to reduce dependency on imports and not only limit the amount of exported foreign currency but support this industry for it to help re-balancing the trade account. For this to happen, there must first be a deep understanding of the needs of this industry and then a commitment from the government and parliament’s side to pass and enforce regulations to meet these needs. This would encourage and attract investments in this sector. Ideally, this plan should also include running calculations that show how many jobs these steps will create. Equally as important is the inclusion of all steps needed to raise trust in the quality of the medications produced locally, both among consumers and physicians. The infrastructure for trust-building from a regulatory and executive level is present as all the factories are certified for ‘Good Manufacturing Practices’ by the World Health Organization, but more investment in this area is crucial. It is worth noting that nearly all the factories are designated producers for international pharmaceutical brands, which attests to their standards. Without further detailing steps, trust-building for quality and the economic viability of this plan are key success factors. In addition to trust-building, local production should be better marketed by physicians who can prescribe trade names from specific manufacturing. Physicians prescribing local products and marketing these products to their patients can greatly support the local market. The need for supporting this industry has been shown in the fears of a lack of equipment in the country at the start of the COVID-19 pandemic. These fears have been temporarily addressed with subsidies.

Concerning pharmacies, their problems – described above - are threefold. First, the pricing mechanism is leading to an overall lower profitability. Second, their overall sales decreased because of diminishing purchasing power. Finally, a significant part of their fixed cost - such as rent - is based on USD, and there is no clear ruling on which exchange rate to follow; most transactions are currently requiring either the 4000 LBP/USD or the 8000 LBP/USD exchange rate. Working on a composite package to tackle these problems is a reasonable and much-needed approach. This would include: adjusting the pricing mechanism, especially for generic medications, and passing regulations that subsidize the pharmacies’ fixed costs (such as rent), like setting the exchange rate for their transactions, waving certain governmental/municipality fees, and providing tax relief.

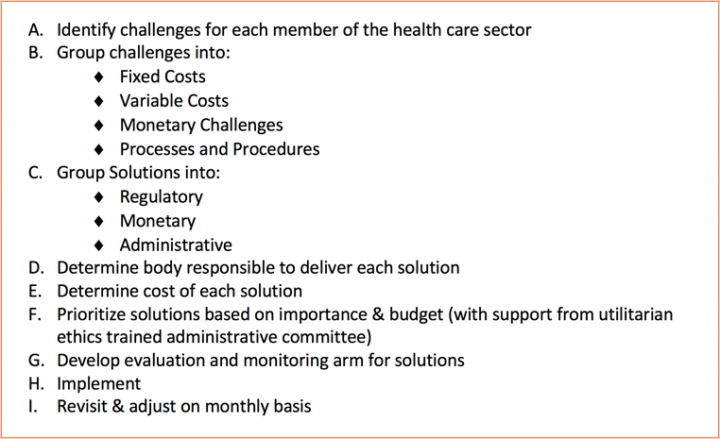

We summarize a general framework of approach to each sector in figure 3.

Figure 3. Framework of suggested approach to the healthcare reform plan in Lebanon during the crisis.

Conclusion

The health care sector in Lebanon is passing through a very difficult period, with the COVID-19 crisis on one hand and the turbulent unpredictability of the Lebanese monetary and financial conditions on the other. In this paper, we highlighted some challenges and suggested temporary solutions. The aim of these solutions is to ensure accessible health care service to the Lebanese and sustain the health care sector during the acute dip pending reaching the steady-state. Ensuring that all steps are performed in an ethical, transparent, accountable, and cost-effective manner is paramount. This can only be ascertained by completing the loop with an arm for evaluation and monitoring. All of this needs to be addressed in a comprehensive plan, while remaining cognizant that in complex systems even minor changes can be either very helpful or very detrimental. The other track in this plan, as mentioned in the paper’s introduction, would be the medium/long term track emphasizing reform from the perspective of financing healthcare, methods of payment for services, and a set of regulations needed to link all the visited aspects with changes on the levels of organizations and behaviours of health care consumers and providers.

Acknowledgements:

We would like to thank Dr. Mona Nasrallah, Dr. Monique Chaya, and Dr. Salim Adib for their valuable feedback on data collected for writing of this paper.

References

Abdo, R. R., Abboud, H. M., Salameh, P. G., Jomaa, N. A., Rizk, R. G., & Hosseini, H. H. (2018). Direct Medical Cost of Hospitalization for Acute Stroke in Lebanon: A Prospective Incidence-Based Multicenter Cost-of-Illness Study. Inquiry, 55, 46958018792975. doi:10.1177/0046958018792975

Al Akhbar. (November 14 2019). The Lebanese pharmaceutical…ًWorldwide quality with competitive pricing. Retrieved from https://al-akhbar.com/Finance_Markets/279257

Ammar, W. (2003). Health system and reform in Lebanon: Entreprise universitaire d'études et de publications.

AMWAL Invest. (2010). Pharmaceutical Sector in Jordan. Retrieved from http://inform.gov.jo/en-us/By-Date/Report-Details/ArticleId/43/smid/420/ArticleCategory/207/Pharmaceutical-Sector-in-Jordan

Banque Du Liban. Intermediate Circular number 535, November 26 2019. Retrieved from https://www.bdl.gov.lb/circulars/intermediary/5/37/0/Intermediate-Circulars.html

Barnes, D. (2020, May 15, 2020). Telemedicine in Developing Countries. Borgen Magazine. Retrieved from https://www.borgenmagazine.com/telemedicine-in-developing-countries/

Brall, C., Schroder-Back, P., Porz, R., Tahzib, F., & Brand, H. (2019). Ethics, health policy-making and the economic crisis: a qualitative interview study with European policy-makers. Int J Equity Health, 18(1), 144. doi:10.1186/s12939-019-1050-y

Central Administration of Statistics. (2020). Key Indicators. Retrieved from http://www.cas.gov.lb/index.php/key-indicators-en

Chen, B., & Cammett, M. (2012). Informal politics and inequity of access to health care in Lebanon. International Journal for Equity in Health, 11(1). doi:10.1186/1475-9276-11-23

Decree number 109 by MOPH, Change in Proportion of Health Coverage, MOPH Website, Decree 109 Stat. (2016).

Deeb, S. E. (2020, July 22, 2020). Crisis hits Lebanon’s hospitals, among the best in Mideast. Associated Press. Retrieved from https://apnews.com/3a4d797c9946e032bbee502c737ee547

Dumit, N. Y., & Honein-AbouHaidar, G. (2019). The Impact of the Syrian Refugee Crisis on Nurses and the Healthcare System in Lebanon: A Qualitative Exploratory Study. J Nurs Scholarsh, 51(3), 289-298. doi:10.1111/jnu.12479

El Nashra. ( July 8 2020). Order of Physicians decides amending medical consultation fee,. Retrieved from https://www.elnashra.com/

Elsunhawy, H. The Lebanese pharmaceutical sector during the economic crisis (A Report) Anadolu Agency. Retrieved from https://www.aa.com.tr/

Epidemiological Surveillance Program, L. M. o. P. H. (2015). Guideline for Medical center, dispensary and field medical unit based sureillance system. Retrieved from

Fair Health. (2020). Healthcare Professionals and the Impact of COVID-19 - A Comparative Study of Revenue and Utilization - A FAIR Health Brief. Retrieved from media2.fairhealth.org

Felzmann, H. (2017). Utilitarianism as an Approach to Ethical Decision Making in Health Care. In Key Concepts and Issues in Nursing Ethics (pp. 29-41).

Friedman, B., & Basu, J. (2004). The rate and cost of hospital readmissions for preventable conditions. Med Care Res Rev, 61(2), 225-240. doi:10.1177/1077558704263799

Fullman, N., Yearwood, J., Abay, S. M., Abbafati, C., Abd-Allah, F., Abdela, J., . . . Aboyans, V. (2018). Measuring performance on the Healthcare Access and Quality Index for 195 countries and territories and selected subnational locations: a systematic analysis from the Global Burden of Disease Study 2016. The Lancet, 391(10136), 2236-2271. doi:https://doi.org/10.1016/S0140-6736(18)30994-2

Hamiye, R. (July 10 2020). Lebanese are at the mercy of the bank and the cartel: the series of drug offenses continues. Al Akhbar Retrieved from https://al-akhbar.com/Community/291262

Harake, W., & Abou Hamde, N. M. (2019). Lebanon Economic Monitor: So When Gravity Beckons, the Poor Don't Fall. Retrieved from

Health, L. M. o. P. (2020). Health Facility Locator. Retrieved from https://www.moph.gov.lb/en/HealthFacilities/index/3/188/8/health-facility-locator

Hemadeh, R., Hammoud, R., & Kdouh, O. (2019). Lebanon's essential health care benefit package: A gateway for universal health coverage. Int J Health Plann Manage, 34(4), e1921-e1936. doi:10.1002/hpm.2850

Khalife, J., Rafeh, N., Makouk, J., El-Jardali, F., Ekman, B., Kronfol, N., . . . Ammar, W. (2017). Hospital Contracting Reforms: The Lebanese Ministry of Public Health Experience. Health Systems & Reform, 3(1), 34-41. doi:10.1080/23288604.2016.1272979

Kohler, J. C. (2011). Fighting corruption in the healthcare sector; Methods, tools and good practices. United Nations Development Programme (UNDP). Retrieved from

Lebanese Customs Administration. (2020). Integrated National Tarrifs. Retrieved from http://www.customs.gov.lb/Tariff/Tariff.aspx

Lebanese Ministry of Public Health. Centers of the Primary Healthcare Network, August 2020. Retrieved from https://www.moph.gov.lb/userfiles/files/HealthCareSystem/PHC/phcc.pdf

Lebanese Ministry of Public Health. (2006-2018). Statistical Bulletins Retrieved from https://www.moph.gov.lb/en/Pages/8/138/health-indicators#/en/Pages/8/327/statistical-bulletins

Lewis, E. (2020, September 14 2020). Lebanon hospitals under threat as doctors and nurses emigrate The National. Retrieved from https://www.thenational.ae/world/mena/lebanon-hospitals-under-threat-as-doctors-and-nurses-emigrate-1.1077418

Malak, A., Hassan, A., & Ferdous, A. (2020). Curbing Financial Corruption in Lebanese Healthcare Sector. Journal of Management Info, 7(1), 10-15. doi:10.31580/jmi.v7i1.1343

McClintock, S., Mose, R., & Smith, L. F. (2014). Strategies for Reducing the Hospital Readmission Rates of Heart Failure Patients. The Journal for Nurse Practitioners, 10(6), 430-433. doi:10.1016/j.nurpra.2014.04.005

Middle East Insurance Review. (2020, March 10, 2020). Lebanon:Non-life insurance sector posts first annual decline in premiums. Retrieved from https://www.meinsurancereview.com/News/View-NewsLetter-Article?id=60582&Type=MiddleEast#

Mikhael, M. (2018). The Lebanese Healthcare Sector: In Urgent Need of Reforms. Blominvest Report.

Mohamed, H. (2018). Exports of medical industries rist to $41M in 5 months Retrieved from https://www.egypttoday.com/Article/3/53318/Exports-of-medical-industries-rise-to-41M-in-5-months

National News Agency. (July 02, 2014). Abou Faour unveils new strategy to audit hospital bill. Republic of Lebanon, Ministry of Information. Retrieved from http://nna-leb.gov.lb/en/show-news/29210/nna-leb.gov.lb/nna-leb.gov.lb/ar

Nayeri, K., & López-Pardo, C. M. (2005). ECONOMIC CRISIS AND ACCESS TO CARE: CUBA'S HEALTH CARE SYSTEM SINCE THE COLLAPSE OF THE SOVIET UNION. International Journal of Health Services, 35(4), 797-816.

Nielsen, J. C., Kautzner, J., Casado-Arroyo, R., Burri, H., Callens, S., Cowie, M. R., . . . Fraser, A. G. (2020). Remote monitoring of cardiac implanted electronic devices: legal requirements and ethical principles - ESC Regulatory Affairs Committee/EHRA joint task force report. EP Europace. doi:10.1093/europace/euaa168

Order of Pharmacists of Lebanon. (2020). Directory of Pharmacies Retrieved July 2020 https://opl.org.lb/pharmacies.php

Quaglio, G., Karapiperis, T., Van Woensel, L., Arnold, E., & McDaid, D. (2013). Austerity and health in Europe. Health Policy, 113(1-2), 13-19. doi:10.1016/j.healthpol.2013.09.005

Salti, N., Chaaban, J., & Raad, F. (2010). Health equity in Lebanon: a microeconomic analysis. Int J Equity Health, 9, 11. doi:10.1186/1475-9276-9-11

Sans-Corrales, M., Pujol-Ribera, E., Gene-Badia, J., Pasarin-Rua, M. I., Iglesias-Perez, B., & Casajuana-Brunet, J. (2006). Family medicine attributes related to satisfaction, health and costs. Fam Pract, 23(3), 308-316. doi:10.1093/fampra/cmi112

Sawaya, R. 1000 pharmacies under the threat of closure, 6 June 2020. Al Akhbar. Retrieved from https://www.al-akhbar.com/

Schellen, T. (2018). A look into Lebanon’s healthcare Retrieved from https://www.executive-magazine.com/special-report/a-look-into-lebanons-healthcare

Statistics, C. A. o. (2019). Health Insurance and Disability Report 2018-2019. Retrieved from http://www.cas.gov.lb/index.php/demographic-and-social-en/health-disability-en

Stuckler, D., Reeves, A., Loopstra, R., Karanikolos, M., & McKee, M. (2017). Austerity and health: the impact in the UK and Europe. Eur J Public Health, 27(suppl_4), 18-21. doi:10.1093/eurpub/ckx167

The Daily Star. (April 15, 2020). Lebanon health sector in critical situation: Haroun. Retrieved from https://www.dailystar.com.lb/News/Lebanon-News/2020/Apr-15/504412-lebanon-health-sector-in-critical-situation-haroun.ashx

The World Bank. (2020a). Macro Poverty Outlook for Middle East and North Africa. Retrieved from https://www.worldbank.org/en/publication/macro-poverty-outlook/mpo_mena#sec1

The World Bank. (2020b). World Bank Open Data. Retrieved from https://data.worldbank.org/

U4 Anticorruption Resource Center. (2020). Corruption and anti-corruption efforts in the health sector Retrieved from https://www.u4.no/topics/health

Wadhera, P., Alexander, T., & Nallamothu, B. K. (2017). India and the Coronary Stent Market: Getting the Price Right. Circulation, 135(20), 1879-1881. doi:10.1161/CIRCULATIONAHA.117.028191

Wim Van Lerberghe, A. M., Nabil Kronfol. (2018). THE COLLABORATIVE GOVERNANCE OF LEBANON’S HEALTH SECTOR. Policy Support Observatory.

World Health Organization. (2020). Global Health Observatory. Retrieved from https://www.who.int/data/gho

The views represented in this paper are those of the author(s) and do not necessarily reflect the views of the Arab Reform Initiative, its staff, or its board.