*This piece is published in collaboration with Chatham House. It is part of a series which addresses the future of governance and security in the Middle East and North Africa, and their impact on the role of the state in the region.

This piece builds on the author’s earlier paper for the Arab Reform Initiative, which examined the impact of the drop of oil prices caused by the Covid-19 crisis on Iraq’s post-2003 political order, characterized by Muhasasa Ta’ifia or sectarian apportionment. This article examines the demographic dynamics in Iraq and their impact on the current system.

Introduction

The new Iraqi government, in place since early May, initial plans to rebalance the budget’s structural imbalance by proposing to reduce the size of the public sector payroll through cuts to benefits/allowances via progressive taxation as articulated by the Minister of Finance, after the crash in oil prices exposed the unsustainability of the current set-up. But the government’s first cuts, minor as they were, were met by fierce resistance from the political elite, which obliged the government to secure the payment of salaries and pensions through linking this with their approval for the state to borrow $18bn to cover the current deficit.

This reaction by the elite, even though all indicators suggest that the public wage bill cannot be sustained and is diverting needed resources away from public investments, is a predictable response given the ethno-sectarian parties’ incentives to protect their patronage networks built over the years through expanding public sector employment. While the elites may be hoping that oil prices would increase in the near future and help fill up the coffers again, in the background, the country’s powerful demographic pressures have been persistently eroding the effects of the ever-increasing spending on the public sector payroll and the buying power of oil rents that have underwritten the system known as Muhasasa Ta'ifia.

Iraq’s population grew 53% from 26.3 million in 2004 to 40.2 million in 2020 (see footnote 1), while its demographic profile exerted, and continues to exert, powerful pressures on its resources given the needs of a young population. The under 25 years of age, which compromised 63% of the population in 2004, grew at a slower rate of 40% in the period to account for 57% of the total in 2020. The country’s slowing high fertility rate of 3.7 births per woman, down from 4.6 in 2004, means that the population will grow 25% by 2030 to 50.2 million. While the under 25 years of age, will grow at a slower 16% in the period, but would still account for a high percentage at 53% of the total.

Demographics in action

Public sector employment was a primary means for building the patronage networks of the ruling ethno-sectarian parties given its dominance in the economy and its role as the largest formal employer. These networks were sustained through increasing the numbers of public sector employees and the amounts spent on salaries and pensions.

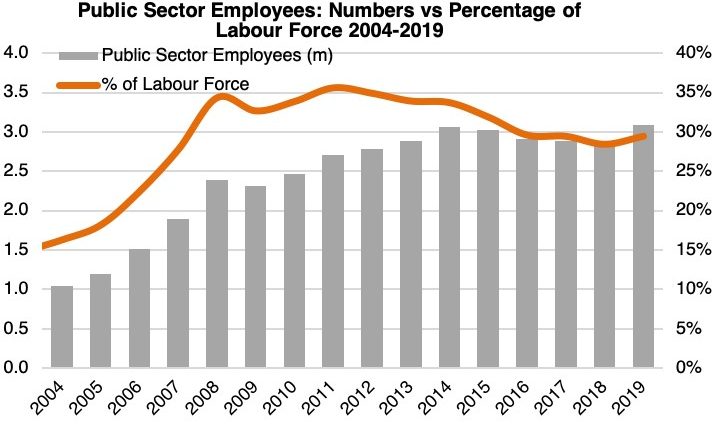

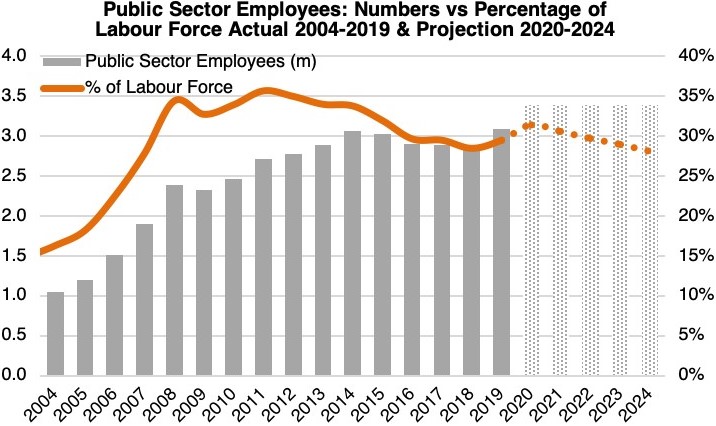

The actual numbers of public sector employees tripled between 2004 and 2014, in the process increasing at a compounded annual rate of 11.3%. However, this was eroded by the compounded 3.5% increase in the labour force which meant that, despite the absolute increase in the number of public sector employees, their percentage of the overall labour force peaked at 35.6% in 2011 and then declined to 33.7% in 2014 (chart 1).

Chart 1: Public sector employees, absolute numbers vs as a percentage of the labour force 2004-2019.

This persistent increase in the number of employees only paused after 2014 because of the combination of the escalating costs of the ISIS conflict and the collapse of oil revenues. This led to a reduction of 5.8% in the number of public sector employees during 2014-2018, while their percentage of the labour force dropped to 28.4%. The growth in hiring resumed its uptrend following the end of conflict and the surge in oil revenues, numbers increased in 2019 surpassing the 2014 levels, but the percentage of public sector employees of the labour force increased only marginally (chart 1).

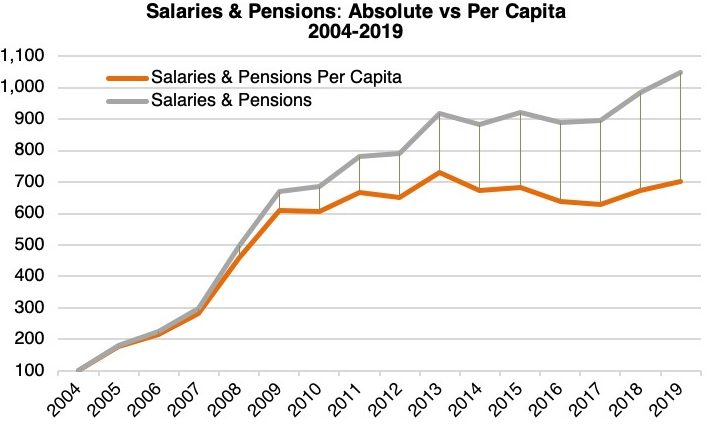

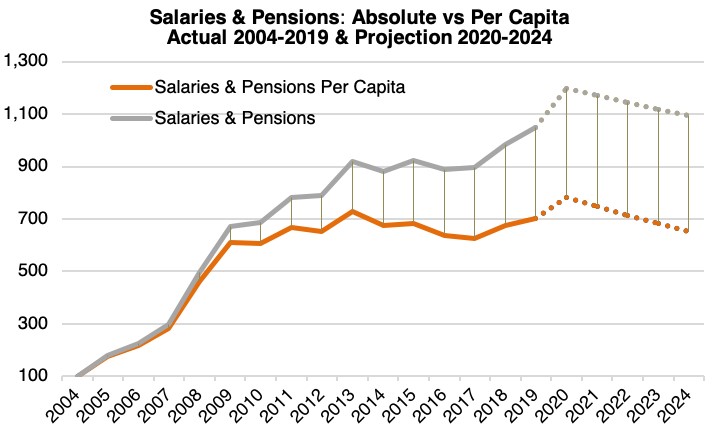

The same demographic erosion was taking place with respect to the amounts spent on salaries and pensions, with the effective peak in spending (on a per capita basis) taking place a year earlier, i.e. in 2013. Compounded growth rates of 27.9% in payments increases by 2013, were eroded by an annual population growth of 2.6%, so that the cumulative effect meant that an increase from a rebased 100 in 2004 to 919 in 2013 was – in per capita terms – an increase to 729. In other words, the demographics have significantly eroded the effective patronage buying power, even though such spending mushroomed over the years (chart 2).

Chart 2: Salaries and Pensions spending in absolute numbers, and in per-capita both rebased to 100 in 2004.

Starting in 2018, the government increased payments for salaries and pension and reversed the first structural reforms that came with the Stand-By Arrangement (SBA) reached with the IMF in 2016. However, here too the demographic erosion was evident. The all-time high of payments on salaries and pensions in 2019, was in per-capita terms 3.7% lower than its peak in 2013 as demographics turned the stagnation in spending during 2013-2017 into a decline in spending per-capita of 14.0% from the peak (chart 2).

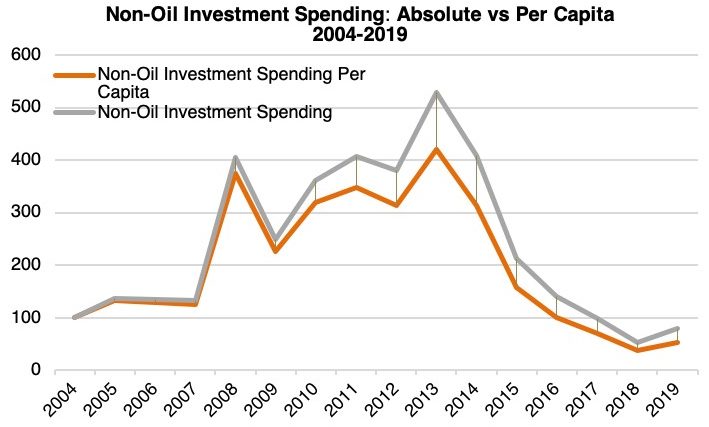

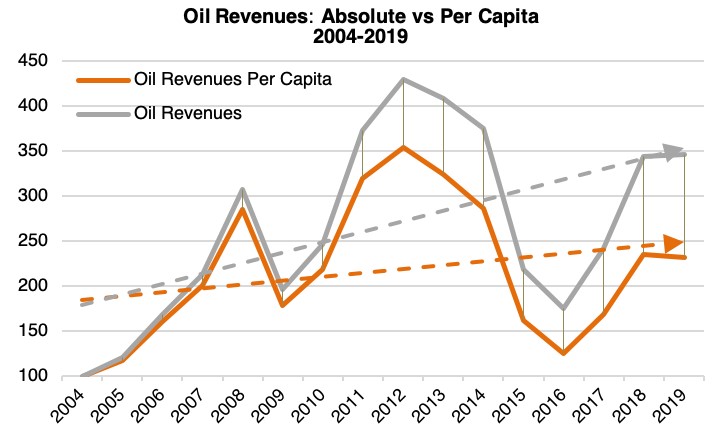

Spending on salaries and pensions far outpaced the increase in oil rents, which peaked in 2012 at 429 from a rebased 100 in 2004, versus the peak in spending on salaries and pensions in 2013 at 919 (charts 2 & 4). In the process, this spending consumed an ever-increasing share of oil revenues crowding out other forms of redistributing oil wealth in exchange for social acquiescence of the Muhasasa’s rule. For instance, spending on education and healthcare quickly plateaued and decreased over the years, and the decrease was particularly notable in per capita terms as a result of Iraq’s demographic dynamics. Such spending is included in non-oil investment spending, the overall patterns of which can be seen in chart (3). This overall reduction in non-oil investment spending has led to a decline of public services, which meant that expanding the public sector payroll was increasingly becoming the only means of building patronage networks for the ethno-sectarian elites.

Chart 3: Non-oil investment spending in absolute numbers, and in per-capita both rebased to 100 in 2004.

Moreover, oil rents are also eroded by demographics. Regardless of the volatility and crash in oil revenues during the crises, the long-term uptrend in oil revenue growth in Iraq, powered by sharply increasing oil production, looks less impressive on a per capita basis and ends up effectively looking like an anaemic uptrend (chart 4).

Chart 4: Oil revenues absolute numbers, and in per-capita both rebased to 100 in 2004, dashed lines are trendlines.

Muhasasa in action

The Iraqi political elite obliged the government to reverse course on its attempts to cut the public sector payroll and pressured it, through parliamentary opposition given the government’s weak parliamentary representation, to marshal all resources to secure payments for salaries and pensions. The government’s need to finance the budget’s deficit through borrowing was only approved by parliament – for $5bn in external borrowing and $13bn in internal borrowings for a total of $18bn – in order to secure payments for current expenditures, including the salaries of newly hired employees, thereby increasing the public sector payroll (see footnote 7).

These measures, however, will only partially serve their intended purpose of preserving patronage networks. It is hard to understand how the government can avoid the negative future consequences of these measures even if we consider the unlikely possibility that, somehow, the 2019 positive economic conditions would continue into 2024 or that the government manages to secure other sources of funding for salaries and pensions as well as maintain spending on other essential government’s expenditures.

Even with a significant increase in spending and in the number of public sector employees as an attempt by the prior government to appease the October 2019 protest movement, the number of public sector employees as a percentage of the labour force will steadily decline because of demographic factors to 28.1% by 2024 – just under the level of 2018 (chart 5).

Chart 5: Dotted line and bars are projections

While, in the same time period, spending on salaries and pensions will be eroded both by inflation and by demographics, so that by 2024 spending per capita will be at 2015’s levels (chart 6).

Chart 6: Numbers rebased to 100 in 2004, dotted lines are projections.

However compelling the demographic argument for seeking real reforms, there is no reason to expect that the governing elite will experience fiscal sobriety, given the perfect track record of economic mismanagement, the lopsided incentives of the post-2003 political order that promote myopic economic policymaking, and crucially the political order’s advanced institutional decay and atomization.

Enter COVID-19

A contributing factor for this behaviour is the belief by the governing elite that this crisis, as severe as it is, will – like all previous crises – eventually pass, and as such preserving past gains outweigh all other considerations.

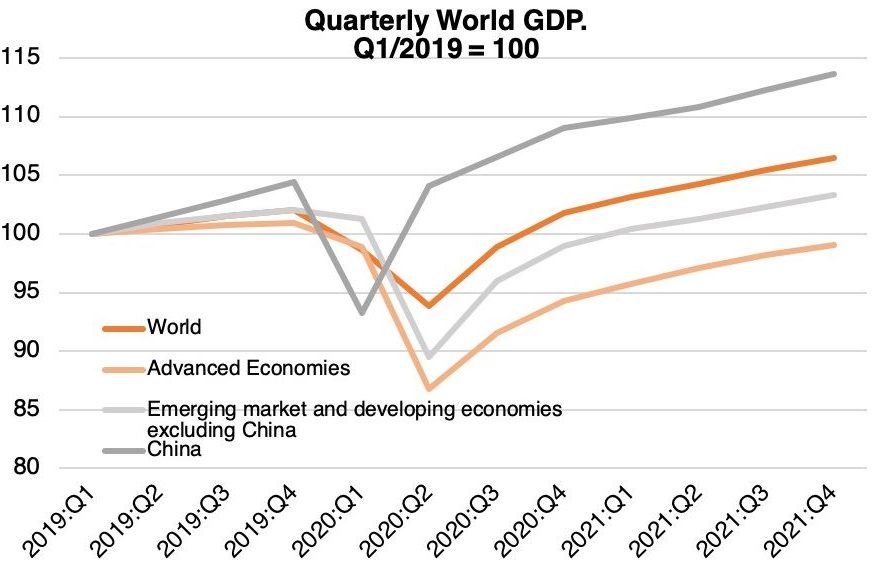

However, the unfolding world order post-COVID-19 calls for a vastly different mindset. As articulated by the IMF in its recent World Economic Outlook (WEO), COVID-19’s negative effects on the world economy were far worse than initially expected. The world economy is projected to decline by 4.9% in 2020 and the recovery would be so slow that even the projected 5.4% growth in 2021 means that world GDP in 2021 is about 6½ percentage points lower than its pre-COVID-19 projections (chart 7).

Chart 7: IMF’s forecast in WEO, June 2020

While there are equally likely either upside or downside projections to this outlook, the extent of the economic damage and the lower productivity (as businesses adopt COVID-19 containment measures) imply that economic activities would remain well below the prior normal until an effective vaccine is administered worldwide. This suggests that at least for the next few years economic growth would be weak at best, and that the whole world will experience the sluggish growth experienced by advanced economies after the 2008 financial crisis.

Therefore, the supply-demand for oil, despite the effectiveness of the OPEC++ historic deal, would be heavily influenced by a likely sub-par demand for at least the next few years. The potential supply abundance of OPEC given its spare production capacity, and the high oil storage levels will, however, keep a lid on oil prices, even after the worst of the crises has passed.

Iraq’s conundrum

For Iraq, this outlook presents its imbalanced budget’s structure with a conundrum that cannot be resolved by current suggested measures, such as increasing non-oil revenues and simple cost-cutting measures such as the ones advocated by the current parliament.

The cost side of the budget is dominated by a rigid current spending component: using 2019 as a base – salaries and pensions would be $50bn of the $80bn current spending budget. Investment spending was $21bn of which oil investment spending was $16bn. It’s very difficult to see the government cutting more than $10bn from the current spending bill given the social factors and vested interests. Similarly, it’s difficult to cut oil investment spending to less than $10bn given the commitments to International Oil Companies (IOCs) and the need to maintain production levels necessary to generate oil revenues. The tiny non-oil investment budget could face the sharpest cuts, but whatever little that is spent is needed to maintain basic services such as electricity generation.

On the revenue side, oil revenues could be about $39bn if Brent crude was to average $40/bbl for the next twelve months and Iraq partly complies with its commitments to OPEC++. Non-oil revenues have a history of playing a distant second fiddle to oil revenues, and even this is oil-related – 25% of the 2019 budgeted figures for non-oil revenues, were from taxes on oil companies and profits from state-owned oil companies. The plans for increasing non-oil revenues from better tax and custom fee collections would be far lower than projected given the economic contraction underway and thus the decline in incomes, profits and imports. Therefore, it would be highly unlikely that non-oil revenues would exceed $10bn at best.

Without a serious reform of the rigid current spending expenditure item, Iraq will be looking at a 12-months’ deficit of around $33bn that needs to be financed. This deficit would continue unless oil revenues rose sufficiently to cover it, but this seems unlikely at this stage for the coming few years.

How can Iraq cover this gap? Iraq is unlikely to be able to raise debt in international markets as its capacity to service such a debt is in doubt given the persistence of this deficit. Domestic sources of funding were saturated during the last crises. This means that the only option is indirect monetary financing, using the country’s foreign reserves, which were $62bn by late June. These reserves could adequately cover the deficit for at least fifteen months before reaching low levels which will likely lead to a forced devaluation. However, these reserves are also needed to support the country’s imports and to meet its foreign obligations. Using 2015-2016 as comparable economic scenarios implies the call on these reserves for imports and other obligations could be about $10bn per year. So, in practice, Iraq would be able to utilize its reserves for the next twelve months or so, before it runs out of resources. After that, it would not be able to meet most of its domestic obligations – topped by a currency devaluation that would further lower the living standards of the majority of the population given the country’s high dependence on imports to satisfy consumption.

A lot of pain now, or much more pain later

The recent developments accelerate the demographic erosion of past gains and argue for the elite to overhaul their modus operandi before an irreversible crisis sets in. Given the response of the political and economic elite in Lebanon’s financial crisis, it is very likely that Iraq’s political elite will, just like their Lebanese counterparts, persist in pursuing the ostrich policy and continue to hope for a recovery of oil prices.

The scale of the past economic mismanagement implies that all solutions to address the size of the public sector, whether radical or gradual, will involve a high element of economic pain that would hit the weak and vulnerable the hardest. Early and real reforms have the advantage of allowing the government to use whatever resources it has, such as foreign reserves, to shield and protect the most vulnerable as much as possible. Moreover, such reforms would lead to a sustainable budget, which opens the door for a resumption of a serious dialogue with the IMF, a rescue package and ultimately allow Iraq to access debt markets.

The rub, though, is that such a reform and the subsequent economic pain will both unravel Muhasasa’s patronage networks and require a buy-in by an alienated population that would, in the words of the October 2019 protest movement, demand upending the whole sectarian apportionment of the post-2003 order.

Acknowledgements

The information in this report is based on publicly available information in web sites, publications, presentations, and research reports as will be seen from the footnote references and hyperlinks. This piece follows from the author’s prior work on the demographic inevitability of the protest movement, and the systematic risks posed by the dependence of on oil revenues. However, the work by Alexander Hamilton has provided the inspiration for the line of reasoning in this piece, and in particular, his yet to be published piece on demographics and Iraq. As such the author would like to express his gratitude and appreciation to Alexander Hamilton. All errors, omissions and mistakes are the author's own.

Disclaimer

Ahmed Tabaqchali’s comments, opinions and analyses are personal views and are intended to be for informational purposes and general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any fund or security or to adopt any investment strategy. It does not constitute legal or tax or investment advice. The information provided in this material is compiled from sources that are believed to be reliable, but no guarantee is made of its correctness, is rendered as at publication date and may change without notice and it is not intended as a complete analysis of every material fact regarding Iraq, the region, market or investment.

The views represented in this paper are those of the author(s) and do not necessarily reflect the views of the Arab Reform Initiative, its staff, or its board.