Executive Summary

- Economic and Political Context

Over the past decade, countries across the Middle East and North Africa (MENA) have faced a succession of crises that have increasingly overlapped and reinforced one another. Protracted armed conflicts in Syria, Yemen, Libya, Sudan, and the Occupied Palestinian Territories continue to disrupt livelihoods and erode infrastructure, while the economic aftershocks of the COVID-19 pandemic have been compounded by global food and energy price volatility, currency depreciation, and rising debt burdens. These pressures are unfolding in a region already characterized by structural labor market weaknesses, high levels of informality, and limited fiscal space. What distinguishes the current moment is not the presence of crisis per se—which has long shaped the region—but the degree to which economic fragility, inequality, and political strain have become mutually reinforcing.

Macroeconomic indicators reflect this cumulative strain. Although inflation rates have moderated in some oil-importing countries, price levels remain elevated relative to pre-pandemic baselines, particularly in contexts where exchange rate volatility has amplified imported inflation (IMF, 2025). In 2024, Lebanon and Syria recorded triple-digit food inflation at 138% and 106%, respectively (WFP, 2024), underscoring the intensity of price instability in conflict-affected settings. Regional growth projections of 2.3% in 2024, rising modestly to 2.8% in 2025 (World Bank, 2025), conceal substantial divergence across countries. Between 2022 and 2024, Sudan’s economy contracted by nearly 40%, the Occupied Palestinian Territories by 30%, Lebanon by 8%, and Yemen by 3% (IMF, 2025).

Fiscal pressures have intensified alongside the slowdown of GDP growth. Indeed, public debt ratios have risen markedly since the global financial crisis and the Arab Spring, and in several countries, debt servicing absorbs a growing share of public expenditure (IMF, 2025). As revenues fluctuate and borrowing costs increase, fiscal adjustment often falls disproportionately on social sectors. Currency depreciation in countries such as Egypt, Iran, and Lebanon has further eroded real incomes (Bennett et al., 2023), while food import dependence and water scarcity heighten exposure to global shocks (FAO AQUASTAT, 2024). In this context, economic vulnerability is not confined to a marginal segment of the population but extends across broad sections of society, including households that would not traditionally be classified as poor.

These economic dynamics are unfolding in a region marked by some of the highest levels of income concentration globally. The richest 10% capture over 63% of national income (Alvaredo et al., 2019; WID, n.d.), and wealth inequality intensified during the COVID-19 period (Kentikelenis et al., 2023). At the same time, nearly half of the population in developing MENA economies lives on less than $8.30 per day (2021 PPP), while extreme poverty has risen in recent years (World Bank, 2025). The juxtaposition of concentrated wealth and widespread economic insecurity is politically salient. Survey evidence indicates sustained dissatisfaction with governments’ capacity to address inequality and economic hardship (Ceyhun, 2019; Arab Barometer, 2024), and protest mobilization has remained recurrent across multiple countries, often triggered by subsidy reforms, price increases, or service delivery failures (Robbins, 2020).

Conflict and displacement further intensify these pressures. Political violence has remained persistently elevated since 2011 (ACLED aggregated data), and as of late 2024, 59.2 million people across the region required humanitarian assistance, with 16.2 million internally displaced (GHO, 2025). In fragile and conflict-affected contexts, social protection systems are frequently underdeveloped or fragmented, and humanitarian responses have often substituted for, rather than strengthened, national systems (IDS, 2025). Yet even in relatively stable countries, economic precarity has become more widespread. Labor markets characterized by high informality, limited unemployment protection and low female participation leave households exposed to income volatility (ILOSTAT, 2025).

The state of social security in the MENA region

It is within this broader political and economic landscape that the architecture of social security systems assumes central importance. Most MENA countries operate bifurcated systems in which contributory social insurance protects a minority of formal sector workers, while tax-financed programs provide narrowly targeted assistance to selected poor households. Effective coverage across at least one social protection benefit stands at 35.8% in Northern Africa and 30% in Arab States (ILO, 2021), with particularly low coverage for children, persons with disabilities, and unemployed individuals (ILO, n.d.). These aggregate figures obscure a more fundamental issue: the design of existing systems assumes that poverty and vulnerability are marginal conditions that can be isolated and targeted. In reality, income insecurity in much of the region is widespread and dynamic.

These structural features mean that income insecurity is not restricted to a small residual population but affects a broad and heterogeneous group. Yet existing social security architectures continue to reflect a model premised on marginal poverty. Tax-financed programs are typically designed as targeted safety nets, intended to supplement rather than anchor social security provision. Contributory schemes, meanwhile, concentrate benefits among formal sector workers, who often constitute a minority of the labor force. The resulting system is fragmented, with limited coordination between programs and significant coverage gaps.

The reliance on proxy means testing (PMT) as the primary mechanism for beneficiary identification reflects this marginal poverty framework. PMT models attempt to infer household consumption or income using observable characteristics—such as asset ownership, housing quality, or demographic composition—rather than direct income measurement. While administratively expedient in contexts with limited income data, such models are inherently imprecise in settings characterized by income volatility and widespread informality (Kidd & Athias, 2020). Empirical evidence from the region confirms these limitations. In Tunisia, 83% of households in the bottom quintile are excluded from the main poverty-targeted program (Ben Braham et al., 2022). In Jordan, exclusion errors reach 67.5% (Anderson & Pop, 2022). In Egypt, more than half of the poorest quintile are excluded from Takaful and Karama (Kidd, 2022). These patterns are not statistical anomalies; they reflect structural misalignment between targeting mechanisms and the distribution of vulnerability.

Beyond statistical inefficiency, targeting can carry political implications. Where eligibility determinations appear opaque or inconsistent, they risk generating perceptions of arbitrariness or favoritism. In contexts where economic insecurity is widespread, exclusion from a targeted program may be experienced not merely as an administrative outcome but as a denial of entitlement. Evidence suggests that poorly functioning targeting systems can erode trust in public institutions (Sibun, 2022), particularly where broader social contracts are already under strain. In Lebanon, for example, where multidimensional poverty affects a large share of the population (ESCWA, 2021), debates around beneficiary selection have become politically charged.

Recent crises have further exposed the limitations of narrowly targeted systems. During the COVID-19 pandemic, most MENA countries expanded social protection coverage through new emergency programs rather than scaling up existing schemes (IPC-IG, n.d.). This reliance on ad hoc interventions reflected both limited institutional capacity and the narrow coverage of pre-existing systems. Transfers were often modest in value and short in duration (Sibun, 2021), providing temporary relief but insufficient income stabilization. In fragile contexts, humanitarian actors frequently delivered assistance through parallel mechanisms, reinforcing fragmentation (IDS, 2025; BASIC Research, 2025). While emergency responses were necessary, they highlighted the absence of robust, shock-responsive national systems capable of absorbing covariate shocks at scale.

Against this backdrop, the question is not simply how to improve targeting efficiency or refine social registries. Rather, it is whether the prevailing model of narrowly targeted assistance is structurally misaligned with the scale and distribution of vulnerability in the region. Where low and unstable incomes affect large segments of society, social protection systems designed for marginal poverty are unlikely to deliver transformative outcomes. The evidence presented in this paper suggests that a transition toward inclusive, lifecycle-based social security systems—combining universal or near-universal tax-financed benefits with contributory insurance—offers a more coherent response to the region’s structural challenges.

The case for life-cycle-based social security

This paper, therefore, argues that a transition toward inclusive, lifecycle-based social security systems offers a more coherent response to the region’s structural conditions. Lifecycle systems are premised on the recognition that income risks arise predictably across stages of life—during childhood, periods of unemployment or illness, disability, and old age—and that these risks are not confined to a marginal subgroup. Rather than attempting to identify the “poorest” through complex and often exclusionary mechanisms, lifecycle systems establish predictable income guarantees linked to clearly defined contingencies.

Such systems typically combine tax-financed universal or near-universal benefits—such as child benefits and non-contributory pensions—with contributory social insurance for formal workers. By broadening the base of beneficiaries, they reduce exclusion errors and simplify administration. Universal or categorical eligibility criteria (for example, age or disability status) are more transparent than asset-based scoring models and less sensitive to short-term income fluctuations.

Figure 0‑1 Multi-tiered lifecycle social security system

Source: Development Pathways depiction

Costs and Fiscal Space

A prevailing concern amongst lower- and middle-income countries concerns the affordability of universal schemes. Many MENA countries are currently facing a severe debt and economic crisis, limiting options in the short run to expand fiscal space for investing in a lifecycle social protection system. Crucially, armed conflict, political instability, and large-scale displacement further constrain the ability of governments to raise revenue, plan over the long term, or deliver services equitably. These crises not only reduce fiscal capacity but also increase demand for social protection—particularly in border regions and areas hosting displaced populations. In these circumstances, governments may achieve universality by designing social security systems to be implemented gradually over time, by initially limiting coverage to a clearly defined group within a life cycle contingency, or by initially achieving universal coverage but with low benefit levels, increasing the benefit value over time.

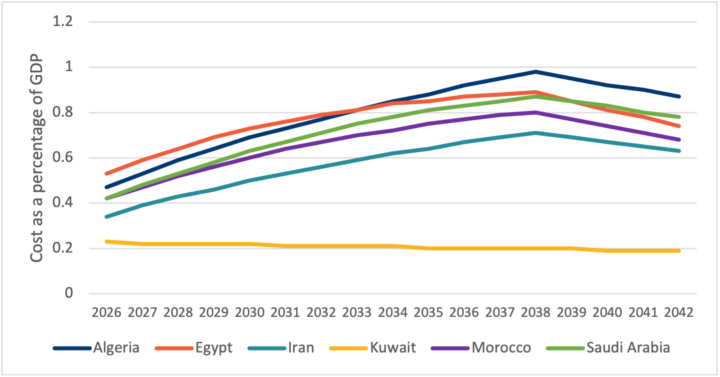

Consider this proposal for Algeria, Egypt, Iran, Kuwait, Saudi Arabia, and Morocco that demonstrates the investment needed for a comprehensive lifecycle social security system under several different contexts. This lifecycle system comprises a basic universal child benefit, universal disability benefits for children and adults, and a universal old age pension for each country. The projected costs associated with the immediate implementation of these core social security components would require a combined investment of approximately 1.94 to 2.72% of GDP in 2026, as illustrated in Figure 5-2. Notably, these expenditures are expected to decline incrementally over time, reaching an estimated 1.5 to 2.44% of GDP by 2042.

Figure 0‑2- Overall level of investment required to establish a universal lifecycle social security system as a percentage of GDP in select countries (2026-2042)

Source: ISSPF costing tool. The figure illustrates indicative social protection benefit schemes across the lifecycle, including child benefits (ages 0–17) set at 4% of GDP per capita; disability child benefits and disability benefits set at 12% of GDP per capita; and old-age benefits (65+) set at 12% of GDP per capita. Values represent illustrative transfer levels used for costing and comparative analysis.

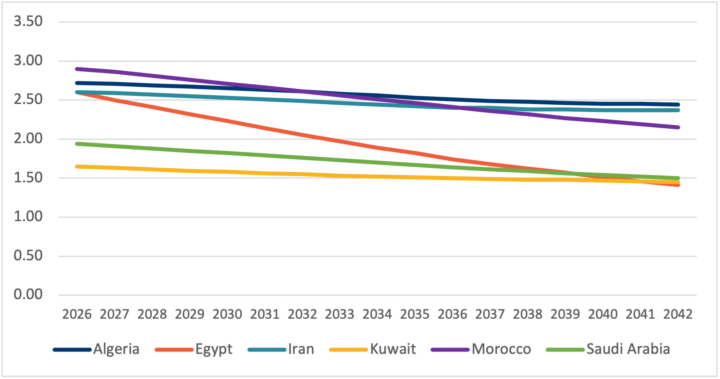

In circumstances where governments face a severe debt and economic crisis, limiting options in the short run to expand fiscal space for investing in a lifecycle social protection system, they may achieve universality by designing social security systems to be implemented gradually over time. Figure 0‑ demonstrates the cost of the gradual rollout of a universal child benefit for Algeria, Egypt, Iran, Kuwait, Saudi Arabia, and Morocco. In this figure, governments start with universal coverage of all children aged between 0 and 4 and gradually increase the upper age limit by 1 year annually until the age of 18. This would require an initial investment between 0.23 and 0.47% of GDP, and each year, governments would increase spending by between 0.01% and 0.07% age points, allowing for the progressive expansion of the scheme. In certain countries, figures remain unchanged for years. In doing so, governments could increase the available fiscal space needed to fund the benefit gradually each year.

Figure 0‑3 Cost universal child benefit as a percentage of GDP, gradually expanded (starting from 0-4 years and increasing the upper age limit by 1 year annually until the age of 18) between 2026-2042

Source: ISSPF Costing tool (2023)

There are several strategies that governments can use to mobilize the resources needed to invest in a financially and economically sustainable national inclusive social security system. This includes increasing tax revenues; re-allocating public expenditures; drawing on official development assistance; fighting illicit financial flows; tapping into reserves; borrowing/ re-structuring debt; and adapting the macroeconomic framework (ITUC, 2022).

In this region, phasing out regressive subsidies presents a major new revenue base for financing inclusive social security. Yet, only a small fraction of fiscal savings made from subsidy reforms have been reinvested into strengthening inclusive social security. Indeed, in Egypt, cuts to energy subsidies between 2014 and 2021 saved 4.3% of GDP, but social security spending only increased by 0.07% of GDP in this period, reaching 0.3% of GDP in total (Friedrich-Ebert-Stiftung, 2023). With an investment of 2.6% of GDP required to establish universal inclusive social security, Egypt's savings could fully fund this expansion. Similarly, in Jordan, investment in social assistance decreased between 2011 and 2017 despite the government eliminating fuel and bread subsidies, which generated 788 million JD (US$1.1 billion) in savings during the same period (Government of Jordan, 2019).

Another potential source of revenue is increasing the rates for progressive forms of taxation, such as progressive income tax, corporate tax, and capital tax (ITUC, 2022). Few countries in the MENA region are effectively leveraging existing tax structures to finance investing in inclusive social security (ITUC, 2022). For example, income tax systems in the MENA region have limited ability to redistribute wealth despite being generally progressive by law. According to a recent IMF study, income taxes in MENA countries raise only about 2% of GDP on average, and revenues vary widely, from 7% of total revenue in Lebanon to 47% in Yemen (Mansour and Zolt, 2023). Minimal revenue generation is in part because of inadequate administration and enforcement, but also because personal income tax systems are generally only progressive for low-income earners. This is due to reduced personal income tax rates for high earners; minimal taxation of capital gains and business income; and increased social security contributions (ibid). Combined, these factors have created tax systems that fail to shift the tax burden onto high-income earners and raise significant revenue. To make personal income tax more progressive and effective at raising revenue in MENA countries, reforms are needed that target high-income taxpayers and sources of capital income like capital gains. These are just two options that governments can use to create fiscal space for inclusive social security. Rouine (2023) presents several other fiscal space options for financing inclusive social security in the MENA region, showing that there is sufficient fiscal space to fill the financial gap needed to finance inclusive social security. Therefore, the amount that countries invest in social security is not related to fiscal constraints: rather, it is a matter of political will.

Impacts of investing in a lifecycle-based social security

Evidence from within and beyond the region suggests that universal or broad-based benefits can achieve substantial redistributive effects. Iran’s universal cash transfer program reduced the Gini coefficient by 2.75 points following its introduction (IMF, 2017). Microsimulation modelling in Tunisia indicates that replacing fragmented targeted schemes with a universal lifecycle system could reduce poverty by 22% (Aboushady & Silva-Leander, 2022). In Jordan, modelling suggests that lifecycle reform could increase consumption among the poorest decile by 10.6% by 2031 (Anderson & Pop, 2022). These findings suggest that universal systems are not merely administratively simpler but can deliver significant poverty and inequality reductions.

Beyond redistribution, lifecycle systems can contribute to macroeconomic stabilization. Predictable income transfers support consumption smoothing, particularly during downturns, mitigating the contractionary effects of shocks. Investment in early childhood benefits has well-documented long-term returns through improved human capital outcomes (Richter et al., 2017). Non-contributory pensions can reduce reliance on intergenerational transfers and support local economic activity in low-income communities. In aggregate, these effects can generate multiplier impacts on domestic demand and, over time, strengthen revenue mobilization.

Imagining a Way Forward

As crises become more frequent and interconnected—ranging from violent conflict to climate-related shocks—the need to ensure social protection systems are fit for purpose in such contexts has never been more urgent. Yet, the prevailing model among many international actors still leans heavily on short-term, externally driven programs that often bypass or even weaken national institutions. While working through national systems during emergencies, particularly during conflict, can be complex and slower, it is also fundamental. Social protection should not be treated as a complementary feature of crisis response—it is a central pillar for enabling recovery, preserving dignity, and reducing long-term vulnerability. Crucially, donor financing should prioritize integration with national systems, with a view toward sustainability and eventual government ownership. Rather than building parallel structures, crisis interventions must reinforce the public institutions that will outlast humanitarian programming. Building resilience means shifting the starting point: supporting national systems from the onset of a crisis, not merely in its aftermath. This requires aligning with existing—sometimes imperfect—social protection frameworks, understanding local context, and recognizing that elements of these systems often continue functioning even amid conflict and instability.

While the socio-economic landscape across the MENA region has significantly shifted in recent years, investing in inclusive, lifecycle-based social protection systems offers long-term developmental and economic gains. The core rationale for universal lifecycle systems is that they are more equitable, efficient, and politically sustainable than narrowly targeted programs. These systems support economic resilience by enabling consumption smoothing, protecting households during crises, and strengthening the social contract through visible, regular public investment. They also contribute to social cohesion in contexts where exclusion and marginalization often fuel instability.

The views represented in this paper are those of the author(s) and do not necessarily reflect the views of the Arab Reform Initiative, its staff, or its board.