Lebanon is suffering the worst economic crisis in its history, caused by the economic model that emerged following the Taif Agreement. The more than two-decade political consensus parceled out state resources among the country’s rival factions - ostensibly under the guise of preventing more civil conflict - while ultimately producing a rentier economy feeding off a corruption-ridden state. The model’s raison d’être - the politics of patronage - presented major obstacles to economic growth and social justice, generated endemic state and non-state corruption, blocked long-needed reforms, and ultimately left the country more vulnerable to external events.

The old economic model is not redeemable. The search is on for a way to set a clear and sustainable economic vision to achieve balanced growth and create job opportunities. Doing so is an absolute and urgent necessity, in order to get Lebanon and its economy back on the right track. A first step in that direction is to stabilize the currency and this paper explores possible pathways for monetary stabilization.

Unsustainable Economic Model

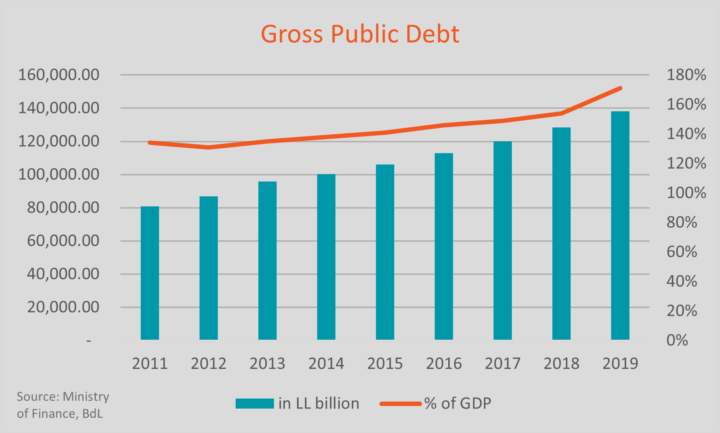

The economic collapse has vindicated in dramatic fashion Robert Mundell’s theory of the “impossible trinity,” which states that you cannot have a fixed foreign exchange rate, free capital movement and an independent monetary policy at the same time - and highlighted the costs of a reckless monetary policy, which depleted foreign exchange (FX) reserves accumulated at a monumental cost to try to maintain a fixed exchange rate and free capital flows. The most visible aspect of this policy was the Central Bank’s (Banque du Liban, or BdL) “financial engineering” operations based on accumulating foreign currencies through borrowing FX funds from local banks at unusually high interest rates compared to international rates. The policy that started in 2012 as a one-off, small scale operation quickly ballooned to unsustainable levels, as the BdL and political class desperately attempted to fund the state (and their clientelist networks) and keep the currency peg, in place since 1997. Political chiefs sought to appease their supporters by expanding the public sector, which ate more of the state budget year-on-year. By March 2020, before Lebanon defaulted on paying back holders of a USD1.2 billion Eurobond, its public debt had reached more than 170% of GDP ) -- one of the highest rates in the world. Yet, despite the unsustainable situation, the monetary and fiscal policies enjoyed consistent political backing, as parties used their access to state resources to fund their clientele networks.

The high interest rates and currency peg dis-incentivized investments in productive sectors and suffocated the real economy, with depositors and investors choosing to keep their money stagnant and in the banks. Meanwhile, an overvalued exchange rate hurt all forms of local production, including agriculture and manufacturing, and led to an over-reliance on imports and chronic deficits in Lebanon’s trade balance. It eroded Lebanon’s competitiveness, increased unemployment, and even wore down productive machinery. This political-economic model turned Lebanon into a rentier economy that relied primarily on a highly vulnerable set-up based on limited services, constant financial inflows from expatriates, illusory profits of banks from financial engineering operations, and returns from over-inflated often unoccupied real estate.

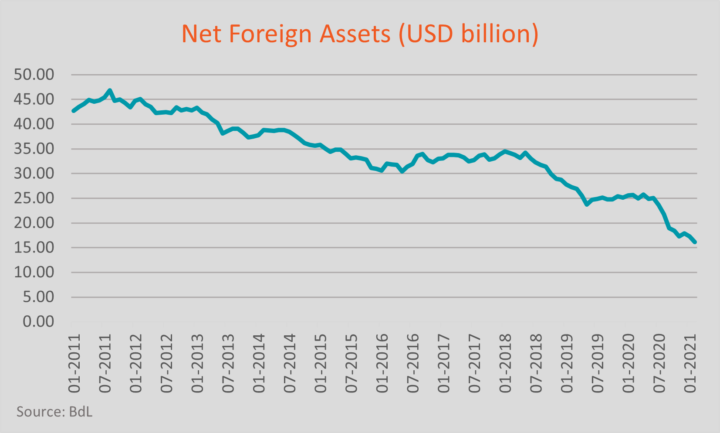

Despite these clearly unsustainable and often contradictory monetary and fiscal policies, the Lebanese economic model was temporarily able to secure large capital inflows between 2008 and 2011, as a new political consensus following the “Doha Agreement” allowed for some stability. Worried by the global financial crisis starting in 2008 and the viability of international banks, the Lebanese diaspora began making large transfers into Lebanon, resulting in a positive balance of payment (BoP). In turn, political leaders used this BoP to defend the economic model as viable, thereby putting off reforms. But cracks in this mirage began to appear in 2011, when Lebanon’s relations with Gulf countries deteriorated over perceived state capture by Hezbollah and the onset of the Syrian conflict. Both contributed to political and social uncertainty in the country and began planting a lack of confidence in the state and its financial stability. They discouraged FX inflows into Lebanon, and the Net Foreign Assets (NFA) began its first uninterrupted decline in Lebanese history. More recently, the mass protest movement in October 2019, the spread of the coronavirus pandemic in early 2020, the governance crisis and the devastating port blast later that year added further strain on the economy.

The Currency Crisis

Lebanon’s “currency crisis” as we know it today is rooted in the economic model described above, and its onset can be divided into a period of decline (2011-2019) which predated the full-on currency collapse (2019-present).

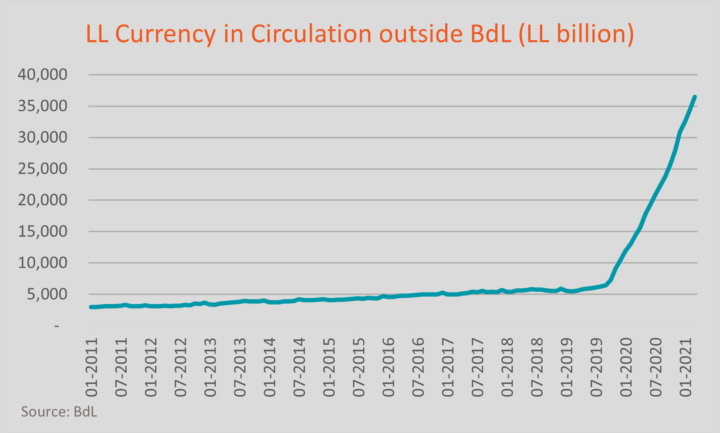

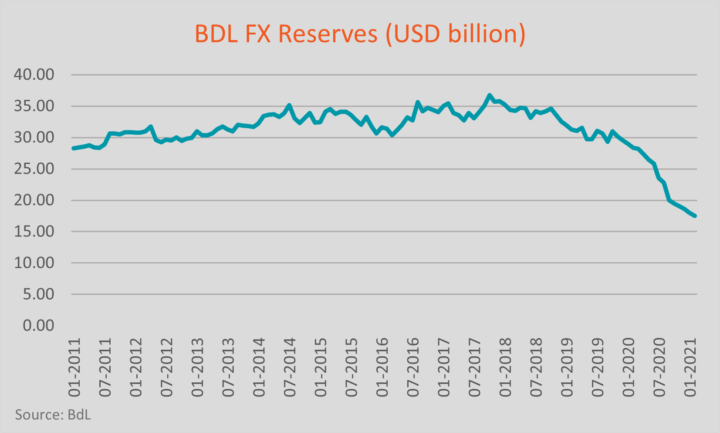

The depreciation that began in September 2019 was, for many Lebanese, the first indicator that something was broken. The Lebanese lira (LL) began to depreciate from its official rate of 1,507.5 to the dollar for the first time in more than two decades. The drawdown on foreign currency reserves at the BdL worsened the collapse and the public’s deteriorating trust in the financial system led to bank runs, currency hoarding and capital flight. In the absence of a capital controls law, banks began imposing their own restrictions on foreign currency and capital transfers, as well as limits on withdrawals of USD or even LL, keeping the door open to all sort of abuses. As a result, BdL’s foreign currencies reserves (excluding Gold, Eurobonds and Foreign Securities) decreased by USD 14 billion since October 2019. As the world shifted towards a cashless economy, Lebanon was spinning off in the opposite direction: currency in circulation outside the central bank increased by 487% since September 2019.

The lira has since depreciated by 90% of its market exchange value, reaching an all-time low of 15,000 LL to USD in the parallel market in early 2021, with extremely volatile periods along the way. There were no serious attempts to control the foreign exchange market, leading to an unregulated multiple exchange rate system. The official rate remains pegged at 1,507.5 LL, while the “Sayrafa” electronic platform, created in June 2020 with the purpose of organizing the erratic currency exchange market and allow the rate to be determined by market forces, has kept its rate arbitrarily fixed at 3,900 LL since its inception. At the end of the first quarter of 2021, BdL announced another attempt to launch a new electronic platform, but it has yet to come online. Meanwhile, the volatile parallel or “black market” rate continues to fluctuate.

In fact, key indicators had been signaling the mounting pressure on the lira and on banks for at least a decade. Lebanon had longstanding twin deficits – in its budget and its current account – but had been accumulating foreign reserves starting in the early 1990s from capital inflows. Its net foreign assets (NFA) steadily increased to reach USD 46.85 billion in August 2011 . But since then, weakening inflows paired with still-rising twin deficits caused the first uninterrupted decline in NFAs in Lebanese history. By February 2021, Lebanon’s NFAs amounted to USD 16.billion, amid dwindling BdL FX reserves.

This decline was the first major red flag, but the multiple underlying causes of Lebanon’s drawdown on foreign currencies are much older and will be discussed here.

First, Lebanon has a dangerously bloated public sector. For the last 27 years, more than two-thirds of government spending has been allocated to current spending. The top costs have consistently included the growing public sector, ballooned by unregulated appointments to feed political patronage networks – including ghost workers – and costly public projects riven with kickbacks. This created an inefficient, wasteful, and unproductive public sector. The problem has worsened since 2017, when parliament approved an increase to public sector wages just months ahead of key parliamentary elections. Lebanon’s recurrent budget deficit grew exponentially and uncontrollably since then, with public spending on personnel costs swelling from 30% of the 2017 state budget to 50% in 2020. Another major drain on the budget was the state-owned electricity provider, Electricité du Liban (EdL), a highly inefficient sector that is inflicting a significant economic and social cost. Over the last decade, the Lebanese government transferred more than USD15 billion to EdL, amounting to an average of 42% of the fiscal deficit over the same period. These costs contributed to an overall rise in the fiscal deficit, which exceeded 11% of GDP in 2019, the last year for which government figures are available.

The second major cost was the quasi-fiscal activities undertaken by the BdL with the endorsement of the political class. Those activities are usually undertaken by tapping on the FX reserves to support what should have been accounted for as government spending, thus further disguising the actual deficit. From 2014 to 2017, BdL introduced successive and sizeable stimulus packages, in the form of subsidized loans. It extended a total of USD6.1 billion of these loans, with almost 59% directed toward the real estate sector. This process, however, was interrupted in the end of 2017, due to abuses and improper use of these loans by some banks.

BdL took advantage of those activities to promote dollarization, thereby creating deposits in USD that are “produced” in Lebanon. Money is created when the banking system makes loans, which in turn create deposits. These so-called Lebanese dollars, or Lollars, are estimated today at USD 53.6billion.

BdL also expanded its use of foreign currency reserves during the first half of 2020, when the Ministry of Economy and Trade introduced a new poorly designed subsidy program, provided to traders and designed to cover the importation of basic goods, including wheat, fuel, and medicine. The program was financed by BdL foreign currency reserves but was exploited politically. It put severe strain on Lebanon’s FX reserves, costing BdL an estimated USD405 million each month. Subsidies to traders and increased inflation led to hoarding of goods, with the vulnerable tranches of the population often not benefitting from the program. The program also gave way to an entrenched smuggling scheme with Lebanon’s most-imported subsidized items regularly ending up smuggled through informal but lucrative networks developed along the porous border with Syria. The smuggling systems have become entrenched over the course of decades and now primarily benefit Hezbollah and its allies on the Lebanese side, and the regime of Bashar al-Assad on the Syrian side.

As a result of the bloated public sector and these quasi-fiscal activities, the government was saddled with a third major cost: its debt servicing. Gross public debt reached 144.6 trillion LL in January 2021, double what it was in 2011. Debt service increased by 50% from 2011 until March 2020, when Lebanon defaulted on its debts. Many slammed it as a disordered default and expected other bondholders to “accelerate” payment of their series, thereby triggering a default across Lebanon’s portfolios. Surprisingly, the acceleration did not take place. Proponents of the decision say it successfully saved Lebanon from further drawdown of foreign reserves and shielded depositors from having their deposits used to pay the external debt as the economy worsened.

All throughout, the Lebanese government’s financial bodies operated with poor governance, and little transparency or accountability. Lebanon did not pass a single budget between 2005 and 2017 and the parliament’s role of monitoring public finances remained non-existent, with the absence of Budget review acts since 2003. Its financial administrators constantly resisted the repeated recommendation of the International Monetary Fund (IMF) under Article IV to float the currency. The IMF had insisted on a floating currency since 2015 as a key and immediate reform measure, but Lebanon’s leaders feared it would reveal the reality of the economic and financial situation and burst the bubble to which the country had tied its reputation.

The result of all these costs, combined with the unwillingness to unpeg the currency, led to unprecedented aggregate losses incurred by the Lebanese government, BdL, and commercial banks, amounting to LL241trillion. ) It also led to an alarming reduction of Lebanon’s foreign currency reserves, which have breached their obligatory threshold, set by the central bank, of USD16 billion. Lebanon is unable to continue with its subsidy program, which will inevitably lead to hyperinflation, shortages and further currency collapse. With the sovereign in default, importers are unable to use any international credit, the private sector had already struggled to access trade and corporate finance in the highly dollarized economy, and now finds itself more squeezed than ever.

Path to monetary stabilization

To recover from this historic crisis, Lebanon must implement a series of measures in the short, medium, and long term in order to achieve monetary stabilization. Such stability would halt its twin deficits, stem the loss in external reserves and reduce uncertainty in economic transactions, therefore spurring long-term economic performance. If accompanied by debt restructuring, financial sector restructuring and fiscal reforms, Lebanon could successfully transition from a rentier, service-based economy to a competitive, open-economy model driven by low tariffs, a flexible exchange rate regime, and a dynamic export sector.

Resolving the distortions and inefficiencies discussed above requires immediate measures that can be implemented within a timeframe of no more than six months:

- Unify foreign exchange rates, with the technical assistance of the IMF, by eliminating regulations and barriers to foreign exchange market operations and establish a transparent foreign exchange platform liquid and efficient enough to allow the rate to respond to market forces. The market making role of the BdL should be reduced and limited to managing volatility;

- Reduce inefficient use of foreign currency reserves through:

- Introduction of a capital control law in line with IMF recommendations to limit the flow of foreign capital outflow while ensuring equal depositor treatment and an end to the ongoing abuses;

- Implement a gradual shift away from the current FX subsidy program, towards direct cash transfers to households as a first step. A study prepared by the World Bank found that shifting to a broad coverage (80% of the population) cash Transfer program will be more effective and efficient. Such a program would improve Lebanon’s balance of payments, meaningfully extend the time-till-exhaustion of remaining BdL reserves, and help cushion the impact on Lebanon’s poor and middle class. In addition, it would help reduce by more than 50% the cost on BdL’s FX reserve. Afterwards, any new subsidy programs should be included in a comprehensive social protection scheme included in the annual fiscal budgets.

- Regain swift control over the money supply and reduce money printing by:

- Repealing BdL’s circular 151, which redeems the Lebanese dollars (Lollars) by printing more money in LL. To successfully do so, Lebanon’s government, the BdL, and banks must, through negotiations, agree on a clear and fair distribution of the LL241trillion ) in aggregate losses incurred by Lebanese entities, with an underlying policy of protecting depositors as much as possible

- Improve public spending efficiency and fiscal revenue collection, as well as fiscal space for an adequate social protection scheme. Lowering the fiscal deficit is crucial since the only way to finance it and continue paying wages of the public sector personnel is through money printing. To do so, clear targets in reducing the size of the public sector and increasing its productivity should be introduced, including through a review of the civil service by an independent international institution and a comprehensive tax reform plan

- Enter into an IMF program in order to introduce foreign currency liquidity, restore confidence, and create the necessary conditions for economic revival.

To maintain long-term monetary stabilization, Lebanon must address its chronic trade deficit. The process has already begun, although involuntarily and as a result of the currency devaluation and loss of household disposable income. The first ten months of 2020 saw a 55% net contraction in trade deficit compared to the same months in 2019, from USD13.5 billion to USD6.1 billion, according to Lebanon’s Customs Authority. Imports of transport vehicles, metals, textiles, and electrical equipment each dropped by more than 50%. Meanwhile, exports of vegetable products increased by more than 30% over the same period.

These trends offer an opportunity to rebalance Lebanon’s trade by decreasing imports and boosting exports. The key to both would be investing in select high-value productive sectors, chiefly agricultural goods (oil, wine, spices, jams) and artisanal products (attire, cutlery, soap). Lebanon’s small production capacity will not be able to compete with imported goods in terms of quantity; rather, its competitive advantage comes from the relatively higher caliber of its products. There is a growing appetite among Lebanon’s population for domestically produced goods, both for economic reasons and for a longstanding tradition of consuming local products. Already, the food and beverage industry has begun opting for local alternatives to raw materials that were once imported. In addition, all productive sectors stand to benefit from the LL’s more competitive exchange rate.

To do so, Lebanon must invest in high-quality and durable infrastructure that would further boost productivity. An effective roadmap already exists in the 2018 CEDRE conference, which secured USD11 billion in international pledges to fund a lengthy list of infrastructure projects, accessible only if the Lebanese government committed to a reform program. Unfortunately, political considerations prevented any progress. Lebanon must begin these reforms, and its international partners must enact a robust follow-up mechanism.

Second, the legal framework required to support private investments as well as Public Private Partnerships (PPP) is missing, outdated, or under-utilized. Lebanon must revise its investment law, develop regulations needed to implement its PPP law, and flesh out other policies and regulatory bodies that could resolve issues such as market concentration and anti-competitive practices.

A major hurdle to Lebanese businesses, particularly start-ups and SMEs, has long been access to finance. This access will be seriously impaired for a significant period of time due to the damage dealt to the banking sector by the economic crisis. Creative, sustainable measures for ensuring post-crisis financing should be laid out. The gap in supply and demand for capital, where equity capital has always played a limited role, must also be resolved.

The aim is for Lebanese products to become more competitive not just locally, but abroad as well, in order to complement import substitution with export promotion. Lebanon already enjoys a national brand identity that is synonymous with high-quality goods, and its millions-strong diaspora presents a ready-made marketing and consuming base. In addition to the steps outlined above, and to maximize the potential benefit to Lebanese businesses, authorities must develop a targeted, well-designed national export policy that incentivizes investment in high-value products. It also requires resuming negotiations for Lebanon’s accession to the World Trade Organization (WTO).

Ultimately, weak institutions, rampant corruption, and inefficiency are the underlying causes of Lebanon’s economic collapse. More broadly, and perhaps more ambitiously, Lebanon must implement broader reforms that are not strictly economic or fiscal. They include but are not limited to: eliminating politicization and corruption in Lebanon’s judiciary, digitizing and modernizing customs processes, and reforming public procurement.

It is important to note here that the author is not advocating protectionism. Import substitution will fail if Lebanon seeks to swap out all or even most of its imports with locally made alternatives, as it lacks the infrastructure and range of raw materials required. Instead, Lebanon should specifically boost high-value products which would otherwise be expensive to import or which have a market abroad, while maintaining low tariffs to encourage trade.

There is growing talk of installing a currency board in Lebanon as the only way to ensure monetary stability. Currency boards – which consist of an independent monetary board that does not engage in any type of discretionary monetary policy and must hold external reserves equal to 100 percent of the local currency in circulation - have indeed proven to be successful in a myriad of countries as part of a renegotiated political consensus, and often paired with a new constitution and other institutional reforms. Lebanon’s political class has repeatedly shown its unwillingness to implement even minor reforms to the country’s monetary regime.

Indeed, while the IMF has recognized the power of currency boards in smaller countries, it has also noted that they require time to build consensus and must be accompanied by “important legal and institutional changes” and that countries with weak banks – like Lebanon – may need a new political consensus before a currency board can be implemented.

Conclusion

The roadmap laid out above is the most meaningful and comprehensive way for Lebanon to put an end to its currency nightmare. However, given the current political class’s unwillingness to enact any serious reform measures in recent decades, its implementation hangs on a new balance of power. Lebanon has a key opportunity – perhaps its only one – to achieve this political shift through parliamentary elections scheduled for the spring of 2022. These elections present the only way for Lebanese to hold their political leaders accountable and could also present an institutionalized pathway to a new government with both the will and capability to engage seriously with the IMF, implement a real reform program, restore confidence, and create the necessary conditions for an economic revival. Under no circumstances should this vote be delayed.

The international community must lean hard on Lebanon’s political players to ensure free, fair, and timely elections next year. If they lack the leverage to do so and Lebanon’s politicians delay elections further, the country will have only one choice left: a new negotiated settlement among current players. While this option presents a smaller window for reform than an institutionalized shift through elections, it does offer the opportunity for monetary stabilization through a currency board. With the same reform-wary politicians in place, a currency board could ensure fiscal discipline and the implementation necessary reforms until Lebanon’s monetary institutions are healthy enough to take on an autonomous policy.

In either scenario, monetary stabilization is a prerequisite towards a new economic model, something Lebanon has sorely needed for decades.

The views represented in this paper are those of the author(s) and do not necessarily reflect the views of the Arab Reform Initiative, its staff, or its board.